OMV Petrom Group: results for Q2 and January – June 2014

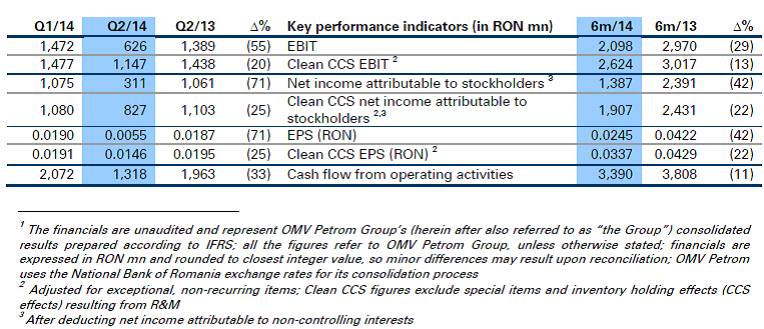

Q2/14 vs Q2/13

- Clean CCS EBIT decreased by 20%, burdened mainly by the one-month planned shutdown of the Petrobrazi refinery and the new construction tax in Romania

- Broadly flat hydrocarbon production in Romania, but lower volumes in Kazakhstan

- Petrobrazi refinery modernization successfully finalized; marketing sales affected by increased fuels taxation and intensified competition

- Negative contribution from power business triggered by deteriorated spark spreads CAPEX up 54%, due to refinery modernization and higher exploration expenditures, the latter reflecting increased activity in the Black Sea

Mariana Gheorghe, CEO of OMV Petrom S.A.: “In the first half of 2014, we continued to implement our CAPEX projects required to achieve our strategy. As such, we successfully finalized the EUR 600 mn refinery modernization initiated in 2010, in time and on budget, which allows us to improve refining margins and better address market demand. In E&P, drilling and workovers contributed to the domestic production stabilization. In the shallow offshore, the Marina-1 exploration well made the largest oil discovery in the Black Sea since privatization. In the deep offshore, we finalized the mobilization of the Ocean Endeavor rig, which enabled us to resume drilling in Neptun Deep, aiming for the Domino-2 well to confirm the initial gas discovery and allow identification of further exploration prospects. The weak demand in oil and gas downstream, coupled with additional taxation introduced in 2013- 2014, almost offset the benefits from gas price liberalization. Nevertheless, given the long cycle of our investments and assuming an investment-friendly fiscal and regulatory environment going forward, we will continue our projects, particularly focusing on field redevelopment projects and exploration, both onshore and offshore.”

Business segments

Exploration and Production (E&P)

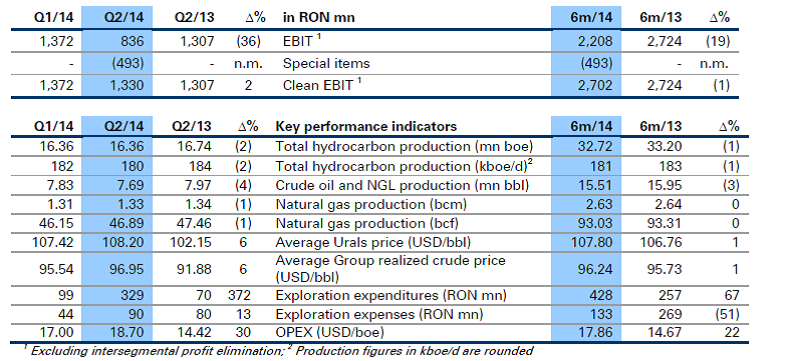

Second quarter 2014 (Q2/14) vs. second quarter 2013 (Q2/13)

- Clean EBIT slightly increased mainly due to higher oil and gas sales

- Group hydrocarbon production decreased 2% on the back of lower contribution from Kazakhstan

- OPEX in USD/boe increased by 30% mainly triggered by new construction tax, higher personnel costs (including one-offs) and lower production in Kazakhstan

- Increased exploration activity in the Black Sea

In Q2/14, the crude price environment continued to be supportive, as the average Urals crude price increased to USD 108.20/bbl, 6% higher compared to Q2/13. The average realized crude price also increased by 6% to USD 96.95/bbl. Clean EBIT slightly increased to RON 1,330 mn, mainly due to higher oil and gas sales, which offset increased operating costs, unfavorable FX rates (USD 4% weaker against RON) and higher exploration expenses. The latter amounted to RON 90 mn, 13% higher than in Q2/13, mainly due to the write-off of unsuccessful wells. The special items reflect the impairment in Kazakhstan mainly due to the unsuccessful field redevelopment results in the TOC fields. Reported EBIT stood at RON 836 mn, 36% below the level of Q2/13. Group production costs (OPEX) in USD/boe went up 30%, triggered by higher costs in Romania, unfavorable FX rates and lower production in Kazakhstan. In Romania, production costs increased by 31% in USD/boe, while in RON terms they were 26% above the Q2/13 level mostly reflecting the new construction tax introduced in 2014 and higher personnel costs (including one-offs) as a result of collective labor agreement negotiations in Q2/14. Exploration expenditures in Q2/14 increased to RON 329 mn mainly related to mobilization of the Ocean Endeavor deep offshore drilling rig for Domino-2 and successful drilling of Marina-1 well in the shallow Black Sea. In Q2/14, we finalized the drilling of 25 new wells in Romania, compared to 39 new wells in Q2/13, focusing on more complex and deeper targets. Group daily hydrocarbon production was 179.8 kboe/d (of which 172.0 kboe/d in Romania) and total production stood at 16.4 mn boe, 2.2% below Q2/13, reflecting the lower production in Kazakhstan. In Romania, total oil and gas production stood at 15.65 mn boe, 0.7% below the Q2/13 level (15.76 mn boe). Domestic crude oil production was 7.03 mn bbl, 1.8% below the Q2/13 level (7.16 mn bbl) due to natural decline in the Suplacu field. Domestic gas production was flat at 8.6 mn boe, mostly supported by the new wells put on stream in the Totea and Mamu fields, which offset the natural decline. In Kazakhstan, production amounted to 0.71 mn boe, 27% lower compared to the same period of 2013, reflecting pipeline integrity issues in the Tasbulat field as well as the natural decline of key fields. Sales volumes were stable compared to Q2/13, as the lower volumes in Kazakhstan compensated higher oil and gas sales volumes in Romania.

Second quarter 2014 (Q2/14) vs. first quarter 2014 (Q1/14)

Clean EBIT decreased by 3% in Q2/14 mostly due to higher operating costs and higher exploration expenses, partially offset by higher gas sales and higher oil price. Reported EBIT, reflected special items in Q2/14 in relation to asset impairment in Kazakhstan. Group production costs in USD/boe increased by 10% in Q2/14, largely driven by higher operating costs in Romania and unfavorable FX rates, partly offset by higher production available for sale. In Romania, production costs increased by 10% in Q2/14, when expressed in USD/boe, and by 8% in RON/boe terms (RON 59.47/boe) mainly due to personnel costs (including one-offs) related to collective labor agreement negotiations. Exploration expenditures increased to RON 329 mn (Q1/14: RON 99 mn) mainly due to increased activity in the Black Sea. Group daily production stood at 179.8 kboe/d while total production was 16.36 mn boe, flat compared to Q1/14, as the 1.4% higher production in Romania was offset by the 22.3% lower production in Kazakhstan. Group sales volumes slightly increased by 1% compared to the Q1/14 level, largely due to higher gas and oil sales in Romania.

January to June 2014 (6m/14) vs. January to June 2013 (6m/13)

In 6m/14, results were driven by stable production and a favorable crude price environment, which led to an average realized crude price of USD 96.24/bbl (6m/13: USD 95.73/bbl). Clean EBIT was broadly flat compared to 6m/13, as higher gas sales and lower exploration expenses were offset by higher production costs and depreciation, as well as unfavorable FX rates (weaker USD against RON). Exploration expenses amounted to RON 133 mn, 51% lower than in 6m/13, which reflected the largest 3D seismic studies in the Romanian waters of the Black Sea. Reported EBIT of RON 2,208 mn reflected the impairment in Kazakhstan, while the first six months of 2013 had no special items. Group production costs in USD/boe were 22% higher than in 6m/13, mainly due to higher production costs in Romania and negative FX development (USD weaker against RON by 3%). Production costs in Romania expressed in USD terms increased to USD 17.59/boe, mainly triggered by the new construction tax introduced in 2014 and personnel costs (including one-offs). Exploration expenditures of RON 428 mn were 67% higher, mainly reflecting increased activity in the Black Sea. Group oil and gas production amounted to 32.7 mn boe while, in Romania, total oil and gas production stood at 31.1 mn boe, slightly below 6m/13. Domestic crude oil production was 14.0 mn bbl, 1.1% lower, mainly due to natural decline in the Suplacu field. Domestic gas production reached 17.1 mn boe, 0.8% higher, mainly driven by the successful offshore workover campaigns and new wells in the Totea and Mamu fields. Oil and gas production in Kazakhstan decreased by 21.8% compared to 6m/13, reaching 1.6 mn boe, mainly due to pipeline integrity issues in the Tasbulat field. Sales volumes decreased by 1% compared to 6m/13 due to lower sales in Kazakhstan partly compensated by higher gas and oil sales in Romania.

Gas and Power (G&P)

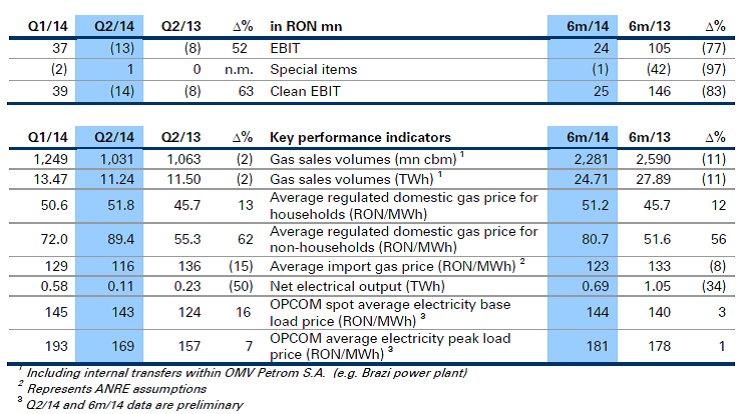

Second quarter 2014 (Q2/14) vs. second quarter 2013 (Q2/13)

- Clean EBIT deteriorated due to negative contribution of power business

- Gas sales volumes slightly lower by 2%

- Low Brazi power plant net electrical output triggered by negative spark spreads

Clean EBIT deteriorated by 63% compared to Q2/13, reflecting the negative contribution of the power business triggered by negative spark spreads, partially counterbalanced by higher contribution of the gas business. National estimated natural gas consumption increased by 3% compared to Q2/13. OMV Petrom gas sales volumes slightly decreased by 2%, reflecting lower sales to the regulated sector and reduced Brazi power plant utilization. These were not fully compensated by the higher demand from the fertilizer industry and broader portfolio of customers. At the end of Q2/14, the total volume of natural gas stored by OMV Petrom amounted to 200 mn cbm compared to 151 mn cbm at the end of Q2/13. In Q2/14, the regulated domestic gas price was RON 89.4/MWh for the non-household sector and RON 51.8/MWh for households, while the average import gas price based on ANRE assumptions was USD 380/1,000 cbm (or the equivalent of RON 116/MWh). The average import quota set by ANRE for the non-household sector was 7% in Q2/14, significantly lower compared to an average of 25% in Q2/13. Romania’s estimated gross electricity production increased by almost 11% versus Q2/13, while the estimated national electricity demand contracted by 1%, with record power exports (1.6 TWh estimated export – import net balance) in Q2/14. Despite higher day-ahead market prices, according to preliminary data published by OPCOM, the increase in the gas price due to the liberalization process led to negative spark spreads in Q2/14. Therefore, the Brazi power plant reached a net electrical output of 0.09 TWh. The plant availability was 93%. In Q2/14, the wind park Dorobantu, with a net availability of 98%, delivered a net electrical output of 0.02 TWh, 19% lower than in Q2/13. For the electricity produced and delivered to suppliers, OMV Petrom Wind Power S.R.L. received ~29,700 green certificates, half of which will become eligible for sale after January 1, 2018 (Q2/13: ~43,000 green certificates, all eligible for sale).

Second quarter 2014 (Q2/14) vs. first quarter 2014 (Q1/14)

Compared to Q1/14, Clean EBIT significantly decreased in Q2/14, reflecting the lower contribution of both the gas and power businesses. Estimated national gas consumption seasonally decreased by 51% versus Q1/14, while OMV Petrom gas sales volumes decreased by 17%. The net electrical output of the Brazi power plant decreased by 83% compared to Q1/14 due to deteriorated spark spreads. Net electrical output of the wind park Dorobantu seasonally decreased by 28%.

January to June 2014 (6m/14) vs. January to June 2013 (6m/13)

Clean EBIT decreased by 83%, mainly due to deteriorated contribution from the power business. OMV Petrom gas sales volumes declined by 11% versus 6m/13, more than the 5% decrease in estimated Romanian gas consumption, mainly due to lower gas extraction from storage in Q1/14 (as the company sold additional quantities during the injection cycle in Q2–Q3/13, instead of storing them for the winter period). In 6m/14, total national estimated electricity consumption slightly decreased by 2%, while the country’s estimated electricity output was 7% higher compared to 6m/13, with the highest increase from renewable and coal generation sources. OMV Petrom net electrical output was significantly lower, reflecting Brazi’s reduced production of 0.64 TWh (6m/13: 0.98 TWh) triggered by spark spreads deterioration on the back of higher gas prices. Net plant availability stood at 95%. With 98% availability, the Dorobantu wind park net electrical output was 0.04 TWh (6m/13: 0.06 TWh), for which OMV Petrom received ~70,000 green certificates, half of which will become eligible for sale after January 1, 2018 (6m/13: ~114,000 green certificates, all eligible for sale).

Refining and Marketing (R&M)

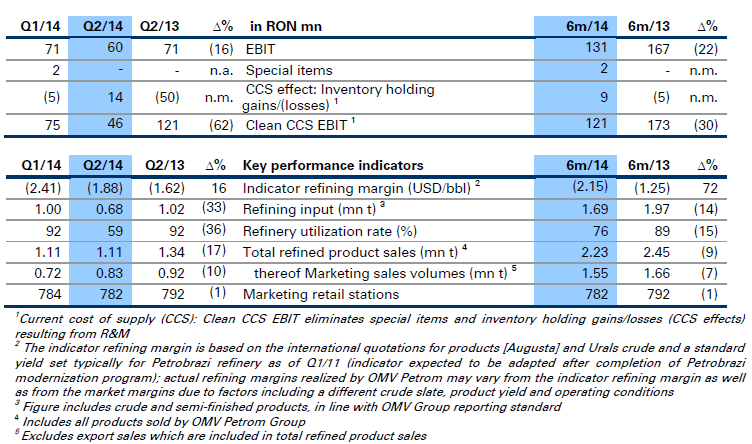

Second quarter 2014 (Q2/14) vs. second quarter 2013 (Q2/13)

- Petrobrazi refinery modernization successfully finalized

- Lower Refining result mainly due to refinery planned shutdown

- Refining margin indicator decreased, triggered by lower fuels cracks

- Marketing sales volumes impacted by increased taxation and strong competition

In Q2/14, clean CCS EBIT decreased to RON 46 mn, mainly affected by the lower throughput as a result of the one month planned refinery shutdown at Petrobrazi, deteriorated refining margins and lower marketing sales as well as margins. The increasing crude oil price and higher product quotations led to a positive CCS effect of RON 14 mn, resulting in a reported EBIT of RON 60 mn. The indicator refining margin was USD (1.88)/bbl, below the Q2/13 level, mainly due to lower spreads for middle distillates, partially offset by higher propylene spreads. The refinery utilization rate stood at 59% (92% in Q2/13), reflecting the planned shutdown. As a result of the latter, the total quantity of refining input in Q2/14 was down by 33% compared to the level recorded in Q2/13. Total refined product sales dropped by only 17%, due to optimized inventory management. Total group marketing sales volumes in Q2/14 were 10% below the Q2/13 level. Group retail sales, which amounted to 70% of total group marketing sales, decreased by 8% compared to Q2/13, mainly impacted by the increase in fuels taxation in Romania and increased competition. Commercial sales dropped by 15% compared to the same quarter last year, reflecting strong competition in the diesel market and higher sales in Q2/13 triggered by the maintenance season and shutdowns of other domestic refineries. Bitumen sales volumes in Romania and Bulgaria were affected by the lack of funds within the construction sector and rainy weather. At the end of Q2/14, the total number of filling stations operated within OMV Petrom Group was 782, 10 units less compared to Q2/13 mainly as a result of retail network optimization in the Republic of Moldova.

Second quarter 2014 (Q2/14) vs. first quarter 2014 (Q1/14)

Clean CCS EBIT decreased compared to Q1/14, mainly due to the planned shutdown of the Petrobrazi refinery in Q2/14. Moreover, the shutdown also prevented the refinery from benefiting from an improved refining margin indicator, influenced by better gasoline spreads. The marketing business result improved in Q2/14 on the back of seasonally higher demand.

January to June 2014 (6m/14) vs. January to June 2013 (6m/13)

Clean CCS EBIT was lower in 6m/14 burdened by the Petrobrazi planned shutdown on both volumes and costs, as well as by the challenging price environment. The indicator refining margin dropped due to lower gasoline and middle distillates cracks. The utilization rate of the Petrobrazi refinery decreased to 76% compared with 89% in 6m/13 due to the scheduled refinery shutdown. Total marketing sales volumes decreased by 7% compared to 6m/13. In the retail business, total sales decreased by 4% attributable to a large extent to the increase in fuels taxation and higher competition. Commercial sales decreased by 12%, as a result of increased competition on the diesel market and higher volumes in 6m/13 triggered by other refineries shutdown. Additionally, the contracted heavy fuel oil quantities were not uplifted due to the mild winter.

Outlook 2014

Market, regulatory and fiscal environment

We expect the average Brent oil price to remain above USD 100/bbl and the Brent-Urals spread to stay relatively tight. The gas and power regulatory framework is undergoing significant changes, with a strong impact on the company’s financial and operating results. In Romania, the gas price for domestic production to be paid by regulated non-household customers in H2/14 was set at RON 89.4/MWh (same level as in Q2/14), with the Q4/14 price subject to further review. The foreseen price increases for the regulated household segment for Q3/14 and Q4/14 have been reconfirmed. Gas demand in Romania is expected to further decline, which will lead to increased competition and margin pressure. Starting July 15, 2014 until December 31, 2018, gas producers have the obligation to sell a certain fraction of their domestic gas production on Romanian centralized markets. Starting April 1, 2014, the basis for the 60% tax on additional revenues resulting from domestic gas sales to non-household customers in the competitive market is the realized price, with a floor of RON 72/MWh for gas volumes sold other than via centralized markets. In the power market, prices are expected to be under pressure due to supply dynamics, with renewables expected to capture a growing share of the generation mix, as well as due to low electricity demand, which partly reflects prospective energy efficiency measures. Starting July 1, 2014, the cogeneration tax for exported electricity was abolished, while for the internal market it was reduced by 45.8% (from RON 18.38/MWh to RON 9.96/MWh). Refining margins and marketing volumes are expected to be further challenged by high price levels for international crude and oil products, together with increased fuels taxation and higher competition in Romania. Given the long term cycle of investments in the oil and gas sector, the recent changes in the fiscal regime have a direct impact on the company’s business. These affect both market supply and demand and also the company’s financials and the operating performance. The tax of 1.5% applied to the gross value of constructions introduced starting January 1, 2014, has a direct negative impact on operating costs in all segments (mostly in E&P) as well as on the business case of some of our investments. Moreover, the fuels excise increases implemented in January and April 2014 put additional pressure on marketing volumes and margins in Romania. We anticipate discussions with the Romanian authorities to achieve a long term, stable and investment-friendly taxation and regulatory framework, discussions that will tackle hydrocarbon taxes and construction tax.

OMV Petrom Group

- OMV Petrom plans to invest over EUR 1.3 bn, of which approximately 85% will be dedicated to E&P (drilling development wells, field redevelopment projects, workover activities / subsurface operations and the Neptun Deep project);

- Strive for high HSSE standards and continue reducing the lost-time injury rate.

Exploration and Production

- In order to stabilize production in Romania, we will further progress field redevelopment, drilling and workovers as well as operational excellence initiatives;

- Continue our intensive operational activities: perform more than 1,600 workovers; drill more than 140 wells, of which more than half are dedicated to field redevelopment projects; bring four redevelopment projects into the execution phase by year-end; 10/23 OMV Petrom Q2/14

- In Kazakhstan – further pursue water injection schemes in both the TOC and Komsomolskoe fields in order to secure reservoir pressure support and slow down the natural decline of production;

- Drill 10 conventional onshore and offshore exploration wells, including exploration drilling under partnerships with Hunt Oil and Repsol;

- Joint-ventures with ExxonMobil: Neptun Deep – drilling at the Domino 2 well started in July, expected completion by end-2014; results to be available early 2015; Midia – continue seismic data interpretation.

Gas and Power

- The gas value chain will be optimized in an integrated manner so as to dynamically address challenges in the market and maximize value creation;

- On July 31, 2014, OMV Petrom closed the sale of the 28.59% participation in the gas distribution and supply company Congaz S.A.;

- Further deterioration of spark spreads is expected, leading to a negative result of the power business in 2014; we aim to mitigate this by consolidating Brazi power plant’s position in the balancing and ancillary services markets, capitalizing on the plant’s flexibility.

Refining and Marketing

- The Petrobrazi modernization program is expected to increase middle distillates yields and improve the refining margin indicator by approximately USD 5/bbl compared to the premodernization period. Moreover, the refinery will continue to deliver on energy efficiency improvements measures;

- Fuel terminal network optimization program: reconstruction works at the Cluj terminal started at the beginning of June with the aim of being finalized in 2015;

- Further pursue cost discipline and optimization of the downstream business.

(www.bvb.ro, August 12th)

Recent Comments