The Country Project: Starting over in the Gas Market in 10 steps

1. CRITICAL ANALYSIS OF THE GAS SECTOR

The day of 31 January 2000 marked the establishment of ANRGN (ANRE predecessor in the gas market), under the management of Iulian Iancu (who is still ANRE coordinator on behalf of the Parliament of Romania), with the declared purpose of reducing gas prices, increasing the quality of services and ensuring the gas supply security.

Targets of gas market liberalization, started in 2000 by ANRGN, were precise, being made public in various publications in the media, by those who started and led this process:

- Low gas price

- Reducing costs for companies active in the gas market

- Consumer protection

- Eliminating crossed subsidies and costs not related to the activity

- Increased professionalism

- Increased productivity

- Increased security in the operation of gas installations

- Eliminating the political or group influences

- Establishing an independent institution to operate in the gas market

- Ensuring a minimum level of energy security for Romania

Circulation of these targets has not ceased in the 15 years that have passed. At first, because they represented goals shared by Romanian authorities, then because they were an obligation of Romania, as EU member state.

After more than a decade and a half, these goals have been reached.

2.1. Low gas price

The first gas market in Europe was established in Transylvania, in 1915-1917, and developed according to the market economy rules until 1948, at nationalization.

In this period, the gas market in Romania operated as a free market, even if the state, through the Ministry of Finance, established the selling price of gas for each gas supplier. Thus, companies developed an active marketing to find new customers and increase productivity to increase profits.

In 100 years of gas sale, the state was the one that established, directly or indirectly, the gas price.

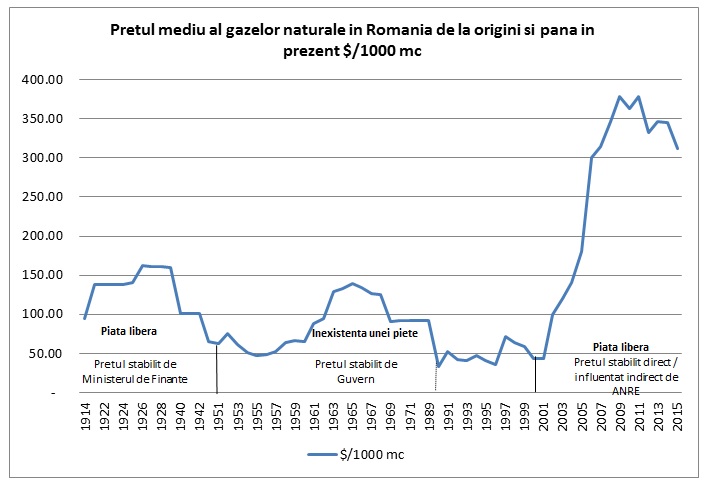

Figure 1. Evolution of the final average price of gas from gas discovery in Romania to date

The price of gas recorded increases and decreases that were influenced by certain events (wars, crises), carried out through politicians.

Corroborating the gas price with the average salary in this period, we can say that there was no correlation between the price of gas and these events (economic crisis, Carol period, war period etc., presenting significant inflections), the state setting the price of gas for other reasons.

After 1948, when the nationalization took place, the “gas supply” met the “demand” imposed by the Communist Party and the Party-State, within five-year plans, in view of a galloping industrialization and proportional development of all areas of the country.

Between 1948 and 1990, one can talk about the public service of gas supply, without having a gas market. After 1990, although this practice continued, in time private capital companies were established, operating in the gas market, determining a demonopolization of gas sales. In this period, the gas price was established by the institutions of the Romanian state.

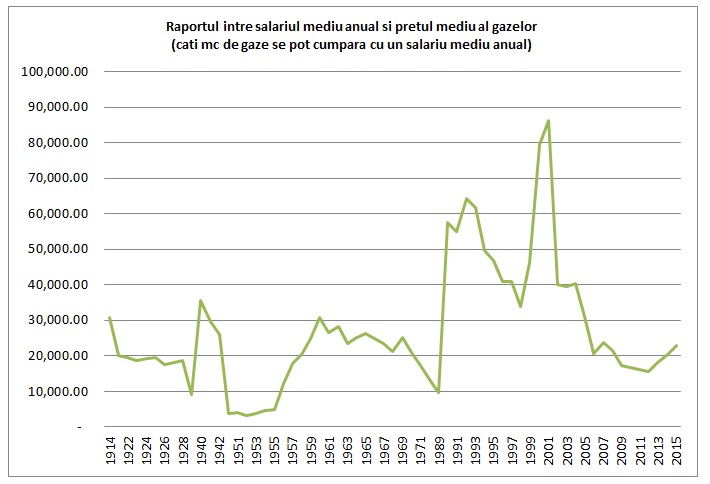

Figure 2. Ratio between the average annual salary and the final average price of gas from its discovery in Romania to date

State “directives” continued during 1990-2000, this time under a pseudo-motivation, invoking social protection. Reporting the average annual salary to the average gas price in this period shows that during 1990-2000 the ratio between the average annual salary and the average gas price presented the highest values in the last hundred years, indicator which contradicts many of the statements and actions taken in the name of social protection.

The idea of gas market liberalization, after 2000, wasn’t implemented through a transparency of activity and development of competition, but by launching the project Gas Price Increase. The graph in Figure 1 highlights significantly this fact. This increase in the gas price was administrative, imposed by state institutions and not by the market. The apparition of the new gas law, in 2012, but especially external requirements, determined the reduction of state involvement in setting gas prices, as of 2016, which determined, timidly, the apparition of a correct trend on the acquisition price of gas by suppliers, keeping the influence of price fixing at the level of the regulated end-consumer.

Thus, we can say that in the past century the state, through its institutions, established an administrative price not related to market realities and without truly protecting those in need.

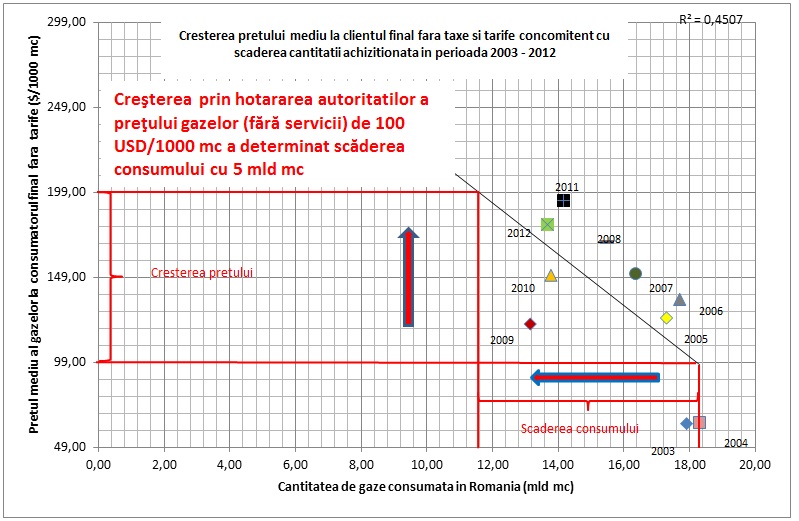

Figure 3. The average price of gas at the end-consumer without taxes and tariffs, in conjunction with the amount of gas sold in Romania

The evolution of the average gas price at the end-consumer increased continuously between 2000 and 2014, the exception being the years 2009 and 2010, when through a political decision prices and tariffs were frozen, or more correctly said a pact was sealed to delay their increase for the following years.

An element still misunderstood in Romania is related to the fact that any price increase determines a decrease in the gas demand in the market. Thus, in a decade of gas price increase by approximately USD 100/TCM determined a decrease in gas consumption by around 5bcm. Respectively there are consumers who are in the impossibility to pay for gas and disconnect, switch to a different fuel or take measures for consumption efficiency. In some cases, these measures are correct. But a situation is reached in which gas systems can become a “labyrinth of death”, in which disconnecting consumers/reducing consumption make the price of gas to increase continuously, all the way to the collapse of the sector.

If we remember the stages of heat distribution systems, we notice that the disappearance of 250 systems (83% of the total) was due to similar situations.

The final price at which gas is sold to the end-consumer consists of domestic and import prices, according to a certain rate, the transmission tariff, the distribution tariff, the storage tariff and various taxes.

In order to analyze the reasons of price increase, we will analyze the manner in which the components that make up this final price influenced this increase, but also the manner in which a component or another influences the price increase.

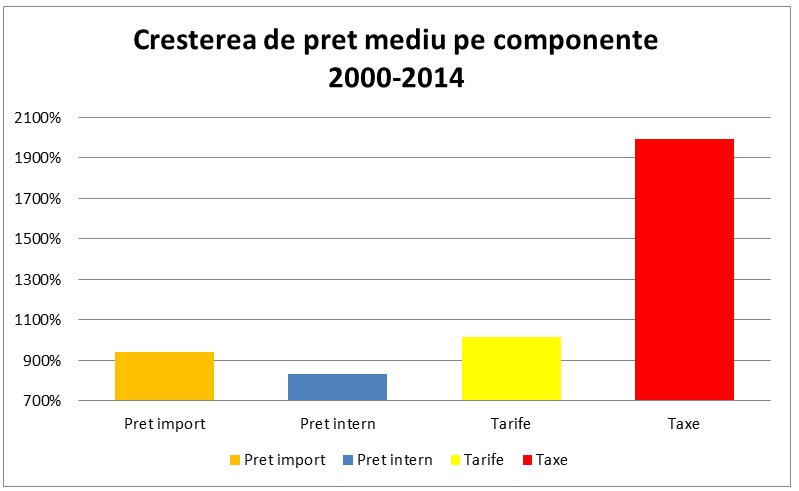

Gas price to the end-consumer mostly consisted, in the analyzed period, of the commodity cost, in a rate of approximately 50% and at the same rate of services and taxes charged by the state.

“In the past decade taxes were the ones that increased the most in the final gas price. Authorities, understanding that taxes from energy sale are among the safest resources to the state budget, preferred to continuously increase them without adjusting them to market realities, being willing to go all the way to sacrificing a sector to get the necessary resources to the budget, to the detriment of certain innovative economic or fiscal measures.

The increase in taxes has primarily influenced the gas price increase.

Figure 4. Increase in the average gas price on components that make up the price

Another important component that influenced the gas price was the increase in tariffs (transmission, distribution, storage), determined by: non-feasible projects put into practice as a result of political influences, the existence of Methodologies for setting the transmission, distribution and storage tariffs based on costs that made these costs to increase continuously in the recent years.

The second factor that determined the increase in gas prices was the increase in distribution, transmission and storage tariffs.

We should mention that most costs found in the transmission or distribution activities are relatively constant regardless of the amount of gas transported. It makes the decrease in the amount transported to determine, based on the existing Methodology, an increase in the tariff to obtain the same revenues as in the years when the amounts transported were higher (the costs remaining the same), aspect which has been found in the recent years.

The pricing methodology existing in Romania is exclusively to the detriment of customers, requesting them the payment of additional tariffs, each time when the amount circulated through the system drops and favors operators that don’t have to take any measure when the amount circulated falls, except asking for higher tariffs.

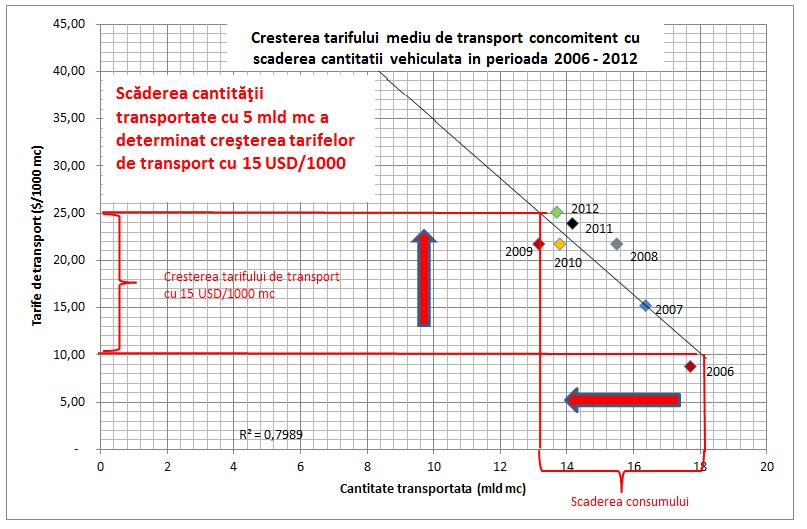

Figure 5. Increase in the average transmission tariff at the same time with the decrease in the amount circulated

In a decade the decrease in the transported gas amount by approximately 5bcm determined an increase in average transmission tariffs by up to USD 15/TCM. The situation is due to the lack of energy strategy repositioning the National Transmission System in the new market conditions, determining changes of legal, engineering and economic nature, including the change of the Pricing Methodology to determine innovative actions of cost reduction, of efficiency and productivity increase, but also the business development to supplement the incomes of the transmission operator.

The decline in gas consumption required an increase in tariffs for the non-restructured sectors to cover the operating costs.

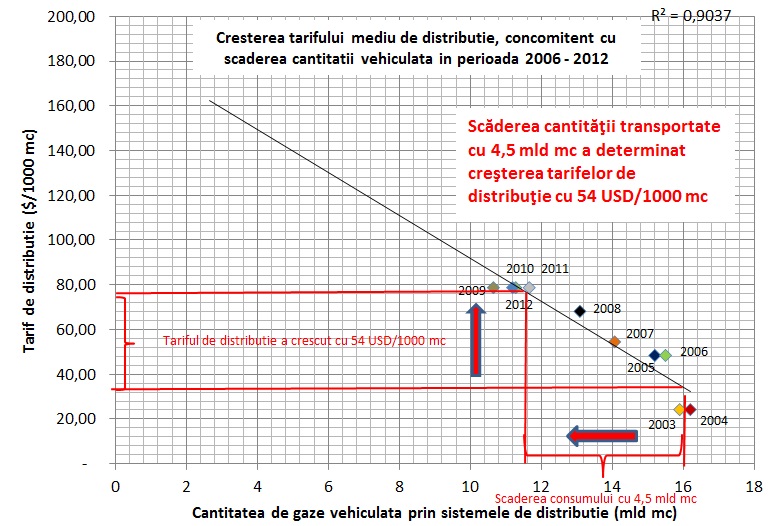

Figure 6. Increase in the average distribution tariff at the same time with the decrease in the amount circulated

In a decade, the amount of gas distributed decreased by approximately 4.5bcm, which determined an increase in average transmission tariffs by up to USD 54/TCM. The methodology for setting distribution tariffs is not intended to determine innovative actions of cost decrease and their reflection in the price to the end-customer. Actions to cut costs incurred by distribution operators after 2005 were not reflected in the price reduction to the end-consumer. Thus, unlike the transmission activity, where there was no significant cost cut program, in the distribution activity, although it existed, it was not reflected in the price to the end-consumer and it will not be reflected in the near future, without several important changes of methodological and behavioral nature.

The decline in gas consumption was used as shield for tariff increase, even at the level of restructured sectors, where costs were reduced.

Creating mechanisms by which the gas price would react to market pressure, in which pricing depends on demand pressure and understanding taxes in the sector as a method to adjust the gas market and the economy and not as main measure to collect money to the state budget will allow hope at the level of gas consumers.

In 2012 the Government of Romania approved the deregulation calendar for gas from domestic production intended for the residential and non-residential consumers, which provided for a slow increase in this price up to the import price level.

The recent years brought the change of the gaseous fuel, integrally or partially (for example, gas is maintained exclusively to maintain a constant temperature overnight), at the level of several consumers. In the next years the discrepancy between the cost of using natural gas and the cost of using other fuels will determine the increase in fuel prices that substitute the gaseous fuel.

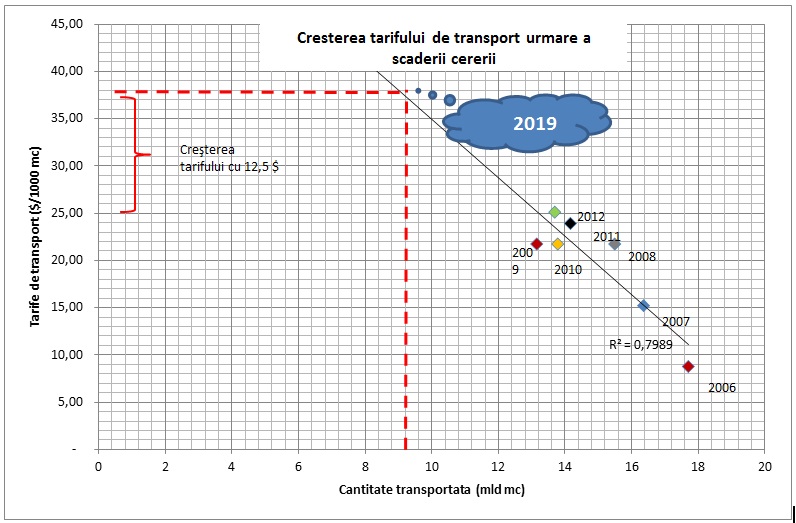

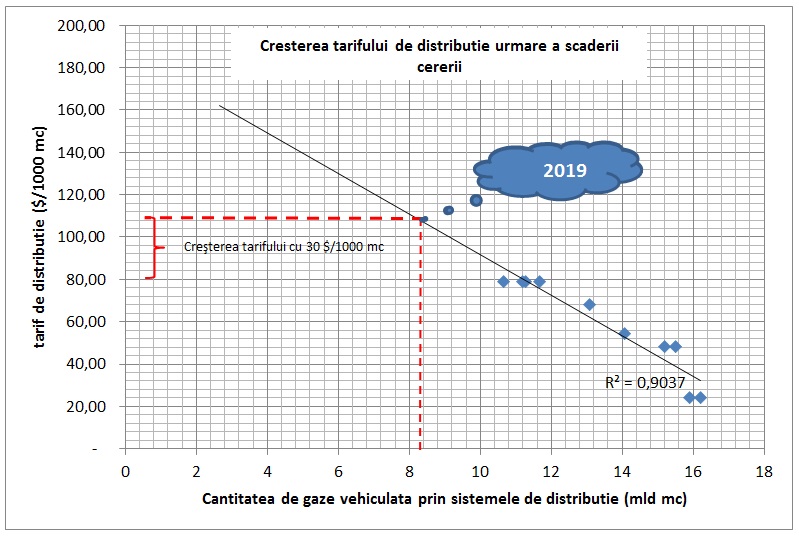

We believe that in the next three years the deregulation process, the behavior in supporting the service tariffs etc. will determine a decline in consumption to the level of 10bcm/year (2020), respectively we estimate that the amount to be transported will be of approximately 9.2bcm/year and the distributed amount of approximately 8.5bcm/year.

Figure 7. Potential increase in the average transmission tariff in the situation of decreasing the amount circulated

Considering the amount to be transported of 9.2bcm/year and maintenance of the current situation (the lack of restructuring of the gas sector), the transmission tariff will have to increase in order to cover the costs by up to USD 12.5.

An important reason of the size of transmission tariffs is due to the low level of use of the network. Costs in the transmission activity being relatively constant and slightly dependent, in Romania, on the transported amount, a decline in the transported amount (of the degree of use) brings the need to increase the transmission tariff to obtain enough incomes to cover the existing costs.

Figure 8. Potential increase in the average distribution tariff in the situation of decreasing the amount circulated

Considering the amount to be distributed of 8.5bcm/year and keeping the current situation, determines the increase in the distribution tariff, in order to cover costs (an increase by up to USD 30).

The same situation is also encountered in terms of distribution tariffs. Costs in the distribution activity are relatively constant and slightly dependent on the distributed amount, thus the decrease in the distributed amount will determine the increase in the distribution tariff to obtain enough income to cover the existing costs.

Changing the market structure, both in terms of the annual demand and the daily and hourly demand, the occurrence of the commercial role of underground storage facilities has determined costs to adapt them to the new requirements.

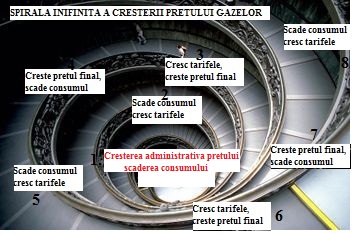

Thus, for the end-consumer, there will be an increase in the price of gas from domestic production, by increasing the transmission, distribution and storage tariffs. If added to this is an increase in the price of gas as commodity for market reasons, we will witness the development of the price increase spiral. Not stopping this spiral and the lack of strategic intervention to redesign the entire gas sector only makes the price to the end-consumer to escalate to dangerous values.

Figure 9. The infinite spiral of price increase in absence of massive change in the gas sector

These increases can be avoided by a structural restructuring at the level of institutions and companies activating in the natural gas sector.

2.2. Reducing costs at the level of companies active in the gas market

Arthur Anderson study, conducted in 1995 (paper realized under the Romanian Petroleum Sector Rehabilitation Project funded by the World Bank), shows that within 3-5 years the Autonomous Gas Administration ROMGAZ had to restructure and organize itself in companies with activities of gas distribution, extraction and transmission. The purpose of this reorganization was based on the separation of costs on types of activities, cost transparency and “surfacing” those costs that were not justified or were very high and forcing their reduction.

Based on analyzes of Arthur Andersen’s company, it resulted that the Autonomous Gas Administration ROMGAZ had to keep its vertically integrated structure, keeping its three main activities (gas exploration-production, transmission and distribution). After the Arthur Andersen project was fully achieved, the Autonomous Gas Administration was expected to become a modern company carrying out its core business on the principle of strategic and administrative business units, at its head office.

Reducing costs at the level of privatized companies in the gas sector was not reflected in the price of gas supplied to the end-consumer.

Contrary to the study’s conclusions, in 2000 the Autonomous Gas Administration split in 5 companies, and in 2005 the two gas distribution companies detached from ROMGAZ, DISTRIGAZ NORD and DISTRIGAZ SUD, were sold to E.ON Germany and GDF France. The owners of the two companies have implemented, after the acquisition, a massive restructuring and cost reduction process (outsourcing, redundancies, negotiation of prices for products and services provided by Romanian companies for them). Thus, it can be appreciated that this principle was fulfilled, but the results were not reflected in a reduction in prices to end-consumers.

2.3. Consumer protection

In the last decade, legislation on the protection of gas consumers has developed significantly. Commercial clauses have been introduced to protect the interests of gas consumers: in the framework service agreements, in regulated supply contracts, performance standards were approved in the provision of services and gas supply to customers etc.

Regulations in force forced gas suppliers to send multiple letters for consumer information.

But the reality shows that they haven’t reached their goal. Gas customers don’t feel more protected today than a decade ago. Most of them feel the lack of protection in relation to gas suppliers, uselessness of any approach regarding gas supplied or services received, abuses they are subjected to by the “gas people”.

Regulations in the field of gas consumer protection have changed substantially, without determining in practice an actual protection of gas consumers.

To a certain extent, this perception is grounded, operators activating in the market managing to place certain regulations by which they can avoid being held responsible by the technique of throwing the blame from one operator to another. But the absence of a real and applicable protection of gas consumers is due to them to a much greater extent. Lack of culture at individual level, but also at the level of companies, determines them to be afraid of suppliers, to refuse to act as a result of own beliefs and to remain unprotected.

2.4. Eliminating crossed subsidies and costs not related to the activity

Eliminating crossed subsidies between various activities in the gas sector, but also between the various categories of consumers, is a fundamental principle in the European Union and was a principle promoted in 2000, with the launch of gas market liberalization in Romania. This principle was corrected in the Romanian gas market by introducing the “gas basket”, a principle through which all consumers were forced to consume gas from imports and domestic production in a similar proportion (given their differentiated prices), to avoid the preferential approach of certain consumers to the detriment of the others. This measure, which was intended to be a short-term one, has suffered various transformations in time, becoming an indirect mechanism for subsidizing certain consumers by other consumers.

The “gas basket” determined industrial consumers to subsidize the residential consumers and vice versa.

The presence of several “gas baskets” for various categories of consumers determined in fact an increase in gas prices for consumers to which a greater amount of the import component was assigned and keeping the price for the other category (residential consumers or industrial consumers have passed, one by one, through these categories).

2.5. Increased professionalism

According to the theory, unbundling activities in the gas sector determines the specialization of persons and companies on a narrow field of activity, determining a substantial increase in professionalism. Competition in the same line of business stimulates innovation and makes prices for services offered to be lower. This theory hasn’t been met in practice in the Romanian gas sector.

The great demand for services in the gas sector, reduced effort – intellectually and physically – to activate in the gas sector, high prices of services determined the quick growth of the number of companies in the gas sector, but also determined the move of persons from various other fields that ceased or restricted their activity, without theoretical training or experience in the gas sector. Thus, thousands of companies received permits and licenses in the gas sector, reuniting tens of thousands of inexperienced people in this activity.

Professionalism in the gas sector has followed a downward trend in the recent years.

Failure to assimilate the specific values of the gas sector, appearances this sector determines compared to its difficulty, lack of time needed for the preparation and training of newcomers from other sectors, cancellation of the hierarchical line, political influence are some of the factors determining the professionalism of recent years to follow a downward trend.

2.6. Lower productivity

Splitting activities ensures the transparency and traceability of actions, but also the way in which these actions are performed in terms of efficiency and effectiveness. Targets set in such a way as to be determinable in space, money and time, subsequently determine the performance of actions allowing to overcome the previous standards.

Productivity is a result, a consequence of efforts taken and in no way is it a feature or skill. Productivity is an excellent indicator of the capacity of gas companies to get additional added values combined with cost decrease.

Labor productivity in the gas sector has followed an upward trend for three quarters of a century, driven by good organization, professionalism, innovation etc., followed by a decrease in recent years. Productivity up in the 90s was a highly monitored indicator, and the battle for exceeding was intense.

Labor productivity represents the efficiency with which factors contributing to achieving the objective are advanced, combined, substituted and consumed. It is expressed by a ratio between results obtained and the amount of human resources “consumed”.

Labor productivity is a result, a consequence of efforts taken and in no way is it a feature or skill. Labor productivity is an excellent evaluator of the capacity of energy companies to get additional added value in conjunction with a significant decrease in prices, contributing to a higher standard of living of the population.

Activity in the gas sector, started in 1910, in Romania, was an entirely new activity, which required staff qualification for the new activity and new technologies: well drilling, extraction, transmission and distribution of natural gas.

In earlier years, labor productivity was significantly influenced by knowledge (quasi-nonexistent) and the technique used (very rudimentary). For example, to build a drilling rig required more staff, more wood, more time etc.

In the operation of gas transmission pipelines, various approaches are found in the early twentieth century. Thus, while for the Sărmășel – Uioara pipeline, they used a lineman every 6.6 km, for the Copşa Mică – Mediaș pipeline they used a lineman every 1.2 km. Although pipelines crossed a relatively similar topography, using a larger number of linemen on Copşa-Mediaş pipeline could be explained by the numerous defects occurred as a result of building this pipeline from recycled pipes from wells in Copşa Mică field.

Labor productivity increased after establishing the General Gas Directorate and especially the Gas Industrial Plant in Mediaş. This evolution was achieved by a hard work of organization, management and supervision of staff, and by developing new technologies. Meanwhile, productivity has progressed strongly.

During the communist period, the gas distribution activity was subordinated to municipalities. Although these communal distribution enterprises faced the lack of money for investment works and even for exploitation works, labor productivity increased in this period compared to the previous one.

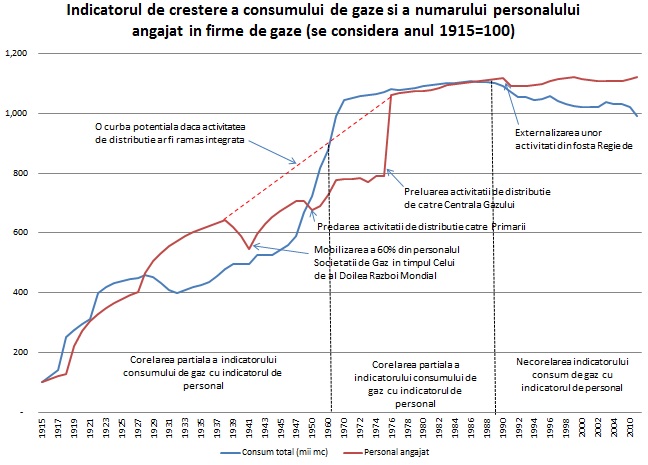

Figure 10. Evolution of gas consumption and the number of personnel hired in the gas sector

The fall of the communist regime in 1989 led to “neglecting” the labor productivity indicator in the gas activity. Although, invoking the increase in labor productivity in the gas industry, starting with 1992, acquisitions were made of equipment, automation, hardware, software, vehicles, test vehicles, special vehicles, telecommunications equipment, radio and telephone, GPS, GIS, mobile phones etc., it followed a downward trend.

We notice that productivity in the production activity is similar to that in 1961, and productivity in the transmission activity is similar to that in 1965, in conditions of much superior technical features.

Productivity indicators in the distribution activity recorded growth after 1990 and decline after the privatization of the distribution activity. The productivity indicator in the gas sector in Romania presents different values compared to West Europe, differences showing a much lower productivity in Romania.

Inventing indicators of productivity determined mimicking added value and did not allow lowering costs in some companies.

The period was characterized by a paradox: people with knowledge were alienated, retired, transferred etc. to hire people who needed time to reach the knowledge of those rejected.

People adopted an attitude at their jobs in line with their own way of perceiving the work environment. The unstable environment destroyed the confidence of people in values such as: quality, innovation, creativity, risk taking, keeping standards and attitude towards work. Work is seen, in general, without interest, to be avoided as much as possible, lacking accountability and tiring.

2.7. Increased security in the operation of gas installations

In the early 2000s in the gas sector it has started the idea of a massive conceptual restructuring. The new approach was based on principles “imported from other countries” (even though most of these principles have been used in the interwar period in the gas sector):

– competition;

– fairness;

– transparency;

with the declared purpose of:

– reducing the direct and indirect costs of using gas.

– separating costs on types of activities and forcing the reduction of those which were very high;

– increasing the quality of services needed for using gas;

– ensuring the customer’s freedom to choose, negotiate and contract various services in the gas sector.

The gas market liberalization has also outlined the idea of a market of services accompanying the activity of using gas:

– design;

– project verification and approval;

– construction of pipelines and installations;

– reception;

– exploitation of installations for using gas;

– verification of installations for using gas;

– expertise.

This situation determined the elimination of certain activities that were previously integrated, but not charged (the cost being included in the distribution tariffs) and the apparition of private companies that execute these works extra charge (additionally to the gas price).

The high demand for services related to user activity, reduced effort – mental and physical – to carry out these works, the high prices of services caused rapid growth in the number of firms that are licensed to perform work in the natural gas sector, and training people in various other fields who stopped or reduced their activity in recent years, without theoretical training and experience in natural gas. Thus, more than 1,500 companies are licensed in performing works in the gas sector, bringing together over 15,000 people engaged in this activity.

Lack of minimum technical culture in natural gas sector among consumers (based on the principle this is fine too, even if their safety and the safety of those living near them is at stake), the impact of additional costs on consumers of gas introduced with these services (costs which were not highlighted/charged by it, until several years ago being included in the tariffs-prices of gas), the large volume of work employed by a company determined an approach of works outside the conditions stipulated by the regulations in force. In fact, demand for this type of services has “perfectly” matched the supply. For a smaller amount, the consumer could benefit from the design and construction of installations from people that sought marketplace, even if they had no experience; for a larger amount, the consumer could benefit from an installation that did not met the requirements of the regulations in force, without being forced to “break” its house and install a larger window. Everyone was happy with this deal, the consumer obtained lower costs and companies gained good money (not being put in the situation of refusing a work).

Thus, one of the purposes of this liberalization of the market of services related to the use of gas, to increase their quality, had the opposite effect (failure to comply with the regulations in force), even the aim to obtain minimum costs for the consumer is apparent, because at the first verification of the installation (until it was realized by distribution operator) the consumer was told it was necessary to remake the installation, according to the regulation, to avoid interruption of gas supply.

In 2011, the obligation that the periodical check (once every 2 years) be performed by the distribution operator activating in the area was removed, the check being allowed to be conducted by any authorized company, which was chosen by the consumer, and thus for a corresponding price one can get the approval for the installation (“sometimes” even if there are some deviations from the regulation).

Starting with 2012, the last link in the intervention of the distribution operator in certifying the safety of the installation was eliminated, so any authorized company can verify and endorse that the project was prepared according to the regulation and that the installation was made according to the project.

When these activities were carried out by the distribution operator, being an unitary approach: design, endorsement, execution, reception, commissioning, periodical verification of the installation and actual realization of the gas distribution, the responsibility was superior both at management level and at the level of the operating staff, because in case of accident failure to properly carry out any of these activities led to the liability of the same operator.

Supporters of principles of activity liberalization, of transparent activities and of fairness, we believe that only the way in which they were transposed in Romania, complicity and duplicity of authorities determined this situation and which in the future can cause an increase in the number and gravity of events.

Mimicking the design, approval and verification of gas installations, so that at a single event the only one guilty is the victim itself, who under the stimulus of insignificant discount assumes: “it will not happen to me“, will increasingly determine the occurrence of hazardous events.

Preventing this situation can be made by:

– amending the secondary legislation and imposing tough restrictions in granting licenses and authorizations and/or tough sanctioning of companies, individuals, institutions that fail to fulfill their obligations/legal duties;

– the reconstruction of certain vertically integrated distribution activities, reuniting the distribution activity and the auxiliary activities specific to the construction and verification of installations, with the regulation of the related tariffs.

15 years ago the end-consumer paid a “regulated” distribution tariff that were several times lower than the current one, even if it included the costs related to auxiliary services related to the construction and maintenance of the installation and connection (costs which today are paid separately and amount to around RON 1,600/household installation) and the number of accidents was lower than today!

Absence of a minimum technical culture in the gas sector, lack of seriousness etc. determined the approach of certain works outside the conditions stipulated by the regulations in force. These aspects are noticeable by the increased number of defects and their impact.

Unbundling and liberalization of certain activities led to the security of installations, in conditions of multiplication of protection systems in the current installations, at an inferior level.

2.8. Eliminating the political or group influences

Gas market liberalization led in fact to increased political influence in the gas sector.

2.9. Establishing an independent institution to operate in the gas market

ANRGN and subsequently ANRE was an institution declared “independent” from its establishment, but in fact it answered the political orders and not only.

2.10. Ensuring a minimum level of energy security for Romania

Lack of an energy security strategy including Romania’s objectives on energy security, anti-energy poverty, energy efficiency, state’s role as majority or minority shareholder in many of the energy companies make the energy notion exist only in the current and past time.

In fact, Romania’s energy security is today “accidental”, and the future is not “too bright”.

What we find today is the result of the approach with gloves!

Market participants believe one thing and say another. The belief that fooling the system, sneaking under the law is the key to success. A continuous evasion, seeking to always fool both suppliers, consumers and authorities. Fear of the future, fear of collapse, do not allow any action.

Failure to apply these principles is due to the Romanian model promoted by institutions that “say one thing and do another”. In this way, Romanians, customers and suppliers, don’t believe in the market economy of “Romanian type”, don’t believe in the liberalized gas market. They don’t feel the market because it is not visible. It is not visible because it is not free. It’s an administrative market, dominated by legal constraints, institutional constraints, operational constraints, constraints, constraints, constraints …!

Being the adept of market liberalization finally means thinking more about the future, without forgetting the past, having the courage of being carried by innovating ideas after getting them through the analysis of sustainability. Delaying the achievement of a real reform of the gas market in Romania will only lead to deeper problems.

2. ANALYSIS OF THE CURRENT SITUATION OF TRADING IN THE GAS MARKET

The activity in the gas sector has to have as main strategic objective the sale-purchase of natural gas, and the other objectives are derived to ensure the achievement of this main objective.

Until 2000 one could talk in Romania about a gas industry, not a competitive gas market, its characteristic being the importance of gas supply to consumers, with a reduced importance of the quality of the gas delivery and contracting process. Characteristic to this period is state monopoly in gas delivery, in conjunction with its obligation to ensure the continuous delivery of gas. At the level of the consumer remained no more than the obligation to pay for gas (often it wasn’t assumed by the consumer either, the centralized economy having the capacity to settle debts through methods specific to the centralized economy). This custom has been passed after 2000, being maintained by the managers of entities who aimed exactly at gas market liberalization, often resorting to the violation or “mistreatment” of the law in order to hide the inability or indolence of consumers that carried out at management level only the “blackmail” of threatening to close the activity and throw people in the street. Inventing numerous instruments with the unique purpose of subsidizing gas prices was another constant concern of entities that should have developed the gas market.

In fact, a great national responsibility for today’s state of Romanian economy belongs to those institutions which through masked subsidies maintained bankrupt gas consuming activities, transferring part of the gas cost to other industrial consumers, substantially contributing to the bankruptcy of the latter. The moment of the crisis in 2009-2012 determined the closure of both consumers maintained artificially in activity, through masked crossed-subsidies, and those that reached bankruptcy as a result of the gas increase policy, including by supplementing these subsidies.

The few ways of operation of the gas market in Romania include the conclusion of bilateral contracts, but which are based on personal relationships between the employees of certain companies that actually make the transactions.

Gas trading in Romania is still made based on personal relationships, the contract being only a formality. Personal arrangements take into account all the problems in the market, lack of instructions and procedures to settle, mediate, solve a problem that would arise in contract performance. Personal relationships make a problem occurred in the performance of the initial arrangement to be quickly agreed verbally and formalized in a contract/addendum to the contract. The lack of a market model in principal, but also of the other elements signaled, make the market to work mostly informally.

Practice used for a long time in Romania in the gas market, where gas was supplied based on verbal agreements, and at the end of the month it was actually known who consumed gas, a contract was formally concluded, backdated, which included everything that happened during the month.

Unbundling the production, transmission, storage, distribution and supply activities determined not only a legal separation, but a deep individualization of various operators, led to the blockage of certain actions, recriminations, misinformation, lack of information/collaboration, failure to harmonize activities, mutual faulting etc., all affecting significantly the gas sale-purchase activity both in normal conditions but especially in abnormal conditions (imbalance between supply and demand, crisis situations). This separation determined, overall, a lower quality of the supply activity (even if there were improvements in certain phases), determined an increase in the gas cost (final price, cost with design, construction, verification, maintenance etc.), determined an increase in the time for building the gas delivery infrastructure.

3. VISION ON RESTORING NORMALITY OF ACTIVITIES IN THE GAS MARKET

The gas sector is characterized by numerous failures, dissatisfactions, abuses, disorientation etc. The fact is that the situation has to change. But How? What? Where? Any vision on the gas sector has to start from the need to rebuild it, from scratch, step by step, by placing the TRANSACTION in the center of the future construction of the new gas sector.

Building a free, transparent, liquid, responsible, closely supervised gas market, developing ways to support vulnerable customers, uniquely dispatched to prevent crises, fully integrated in the European Energy Union and promoting the sustainable development of gas resources.

All activities in the gas sector (design, construction, exploration, exploitation, services related to gas handling) must have a single purpose, of facilitating gas trading in order to obtain the best gas prices at a certain point and for a certain quality of delivery. Thus, it is necessary to immediately get out of the custom of the last 16 years, in which the activities related to supply became core businesses and the supply activity became an associated business. The project “gas market liberalization” carried out in the last 16 years lost sight of the objective of the market, to sell-purchase gas and the need to realize certain activities for this goal: exploration of fields, extraction of gas, developing a certain form of storage, the design and construction of pipelines, exploration of objectives in the sector, dispatching, metering, allocation etc.

Placing the transaction as the existential purpose of the gas sector is the starting point of building the way in which the other activities in the gas sector will be carried out.

Thus, it is necessary to understand that:

- The primary and secondary legislation, for all activities in the gas market, need to have as purpose the development of trading;

- Full transparency on the activities carried out in the gas sector (without affecting confidentiality), activities, amounts, costs, prices, penalties etc.

- Detailed and continuous dissemination of the modality of performing transactions, of carrying out the activity of design, execution, operation of pipelines not as an end in itself, but with the only goal to develop the market, to increase the number of transactions and volumes traded, to increase the degree of use of infrastructure, determining all actors in the gas sector to act with the purpose of favoring gas trading;

- Computerization of the gas sector, to ensure the quick and detailed access to information supporting transactions, market development, increase in gas demand, cutting costs with the associated activities;

- Establishment of an institution to settle disputes in the gas market (SAL), as autonomous, non-governmental, apolitical legal entity, of public interest, whose activity is the mediation of conflicts in the gas market;

- Creating a specialized and powerful department for the Gas Consumers Protection, within the National Consumer Protection Authority (ANPC), which would take action and respond quickly and in a professional manner to all complaints of gas consumers, in order to defend them, to prevent unlawful actions of suppliers and harshly sanction abuses;

- Creating a specialized and powerful department in the gas sector, within the Competition Council, which would quickly take action to any potential dominant position in the market, in order to prevent, protect, maintain and boost competition, and harshly sanction deviations from the competition principles;

- Professional, independent ANRE, removed from political influence and groups of interest, able to act in the interest of gas market development;

- Introducing a set of best practices (energy governance) at the level of all entities, regardless if they carry out main, secondary or related businesses in the gas sector, in order to develop transactions, increase competition and integrity in the gas market;

- Eliminating the regulated market and developing support programs and especially for the reduction of the number of vulnerable consumers (actually vulnerable);

- Infrastructure (production, transmission, distribution etc.) has to be designed, built, exploited in such a way that it meets any type of transaction, answer to market requirements in an efficient and effective way, not being a “stone at the supply’s throat”, no longer consuming unnecessarily the intrinsic value of natural gas;

- Defining an entity (the National Authority for Dispatch and Energy Security), with legal access to all data in the energy sector, subject to confidentiality, and preventing crisis/emergency situations by the entirety of energy issues (gas, oil, electricity, coal), sending the appropriate warnings and having the competence to intervene in crisis situations for the appropriate dispatch of all sources available (of all forms of energy in an unitary way), to properly overcome them.

4. THE PROJECT OF FORMING A FREE AND FUNCTIONAL GAS MARKET

Vision on the gas market has to go through several stages, which have to be built and implemented gradually, within a clear deadline, correctly established, admitting the tolerance of gas sector operation until that moment. The most difficult aspect will be determined by the reluctance to change of both the persons concerned and of the disinterested (consumers, employees). Added to this is the destructive influence of the lack of unit, cohesion, patriotism (sometimes, in the past, going all the way to actions to undermine some against others) of institutions that have the obligation to determine the future of Romania (Government, Parliament, Presidency).

We divided the project in several sections, which have to be realized:

- Construction of the legal framework ensuring a free and functional market,

- The Natural Gas Code (rewriting the Gas Law and interventions on the related legislation).

- Eliminating the regulated gas market.

- Forcing gas producers/suppliers in Romania to publish Best practice guides on gas sales.

- Completing the competition legislation and procedures for urgent investigation of these anticompetitive practices

- Best practice guide for the allocation of metered gas

- Introducing the notion of daily reserved capacity in the existing points on the entire chain production-transmission-distribution

- Rewriting the Transmission Network Code

- The Distribution Network Code

- The Storage Facilities Code

- The Natural Gas Market Code

- Establishing the Balancing Operator.

- Introducing mechanisms to ensure flexibility and functionality of the market.

- Developing cheap guarantee schemes

- Computerization of gas market activity

- Methods and measures for the protection of vulnerable consumers

- Governmental strategy for protecting vulnerable customers

- Appointing an institution to apply and coordinate the protection of vulnerable customers

- Best practice code for licensed suppliers in supporting vulnerable customers

- Legislative changes in order to reduce the number of vulnerable customers (prepayment of gas, flattening the monthly curve of gas payment).

- Rethinking the activity of design-execution-operation of objectives in the gas sector as action intended to boost transactions

- Rethinking the system for the authorization of persons who are active in the field of design and construction

- Eliminating multiple specializations at the level of the same person

- Setting the incompatibility between the activity of design, verification and examination at the level of the same person

- Obligation of examination by independent experts of works in the gas sector in conditions of opportunity, usefulness, feasibility, reliability, security, safety.

- Rethinking the philosophy of norms

- Rethinking performance standards

- Rethinking the philosophy of distribution systems

- Re-engineering of the transmission system

- Re-engineering of the storage activity

- Rethinking the pricing methodologies

- Supporting the establishment of the Gas Engineers Union, a professional entity responsible for the professional preparation, training, development and sanctioning

- Strengthening/establishing institutions with responsibilities in ensuring the functioning of the gas market

- Establishing a center of mediation and quick settlement of disputes in the gas market (SAL)

- Establishing a center of information and dissemination of information on the gas market

- Changing the organizational behavior of institutions with responsibilities in the gas market

- Specialized department for the Gas Consumers Protection, within the National Consumer Protection Authority (ANPC), with procedures allowing them self-referral and respond quickly and in a professional manner to all complaints of gas consumers, in order to defend them, to prevent unlawful actions of suppliers and harshly sanction abuses

- Specialized department within the Competition Council, with procedures allowing them to quickly self-refer to any potential dominant position in the market, in order to prevent, protect, maintain and boost competition, and harshly sanction deviations from the competition principles.

- Establishing the National Authority for Dispatch and Energy Security

- Establishing an entity with role of National Authority for Dispatch and Energy Security unique for all forms of energy

- Fulfilling the role of Competent Authority (CA) in the gas sector, ensuring the security of offshore activities, establishing and maintaining a minimum level of reserves of oil and petroleum products

- Integrating Romania in the Energy Union regarding the gas market

- Appointing the entity responsible for Romania/s integration in the Energy Union

- Drawing up the strategy of integration in the Energy Union

- Human resource development and improvement in the gas sector

- Appointing the entity responsible for the security of human resources needed for the operation of the gas sector

- Developing programs for studies and training in accordance with the requirements of the gas market

- Developing training programs in accordance with the requirements of the gas market

- Developing investments and eliminating investment barriers in the gas sector

- Eliminating limitations on access to land

- Eliminating limitations that make impossible the use of public roads for the construction of gas objectives

- Simplifying the approval and permitting processes for investment works

- Harmonization between the laws on energy and other Romanian and EU laws

- Stability of the legislative framework and predictability in the energy sector

- Public policies in line with Romania’s interest

- Rethinking the management of state ownership and private management for companies with state capital in the gas sector

- Imposing a unitary Energy Governance in companies and institutions in the gas sector.

5. CONSTRUCTION OF THE LEGAL FRAMEWORK ENSURING A FREE AND FUNCTIONAL MARKET

It is necessary to rebuild the legal framework ensuring a free and functional market, starting from scratch, eliminating the non-harmonized and incomplete primary and secondary legislation existing today. We will present the main items, which we consider necessary to normalize the activity in the gas sector.

- The Natural Gas Code

In order to eliminate the approach of a regulatory document for each activity, which makes certain operators accuse that an act does not concern them, we propose the development of a Gas Code, containing both the primary legislation and the secondary legislation and introducing the implementing rules and procedural sheets, so that legislation addresses all actors, so that they all have the final target of performing gas transactions, at a high qualitative level and in conditions of maximum safety.

- Eliminating the regulated gas market.

The free market can only work by eliminating indirect subsidies, restrictions, manipulation, arbitrary intervention, today imposed even under the Gas Law. It is necessary to eliminate all legal restrictions that allow direct or indirect price “manipulation”: the gas basket, the producers’ obligation to make available, regardless of circumstances, regardless of contracts, gas for regulated consumers, state intervention in setting the price for the domestic producer, to eliminate interventionism an ensure market functioning.

- Forcing gas producers in Romania to publish Best practice guides on gas sales.

In order to develop the gas market in Romania it is necessary to increase the volume of transactions by increasing diversification and the number of gas packages sold in the market, in order to cover the entire range of requests in a market. Given the practice of the recent years, publishing such a Guide will bring benefits for the market and producers.

- Completing the competition legislation and procedures for urgent investigation of these anticompetitive practices

It is necessary to supplement the existing competition legislation with new regulations to prohibit certain practices currently existing in the gas market and which determine market manipulation, anticompetitive agreements, concentration of power to sell by using the satellite suppliers etc., stimulating complaints against such practices, self-referral of institutions controlling anticompetitive practices and boosting actions of investigation of such practices.

- Supplementing the primary legislation with new mandatory concepts for gas market functioning

It is necessary to supplement the primary legislation with new concepts, absolutely necessary for gas market functioning:

- allocation of amounts supplied, transported, distributed, stored

- swap of gas amounts, as virtual trading activity, in conjunction with the backhaul service on transmission, distribution and storage systems

- reverse flow in entry/exit points of transmission systems, as operation for bidirectional flow of gas, if this technical possibility exists (operation met in the interconnection points with other transmission systems or with the upstream pipeline systems).

- Backhaul in entry/exit points of transmission systems, as operation for bidirectional flow of gas (operation met in the interconnection points with other transmission systems or with the upstream pipeline systems).

- redefining the Transmission System, with legal changes, royalties, licenses, transmission network codes different for each of the future types of transmission that will occur.

- defining the instruments of flexibility and guarantee in the gas market.

- Best practice guide for the allocation of metered gas

It is necessary to develop a Best Practice Guide containing Mechanisms for the allocation of amounts sold, stored, transported, distributed, allowing the fairness of operations and especially the entry into legality of these operations, respectively compliance with the Civil Code (art. 1674 and art. 1678) on the modality of individualization of generic goods, such as natural gas.

- Introducing the notion of daily reserved capacity in the existing points on the entire chain production-transmission-distribution

Introducing the notion of daily reserved capacity in the existing points on the entire chain production-transmission-distribution, in order to allow the unitary approach of this notion and the real functioning of the market for capacities. We believe it is necessary to eliminate the hourly capacity reservation (currently used in the transmission system), as long as it cannot be monitored throughout the sources-consumption chain.

Determining the capacity in all entry-exit points in/from the production/transmission/distribution/storage facility systems. When we discuss about capacity, it can only be addressed in a unitary form, the technological/ technical/ marketable/ contracted/ used/ unused/ uncontracted capacity. It is necessary to display the updated situation of these capacities and develop the mechanisms to trade capacities, and to monitor the efficiency of using them. This approach is the real way of streamlining the activity of capacity management, which is more than in excess in Romania, thus determining the possibility to reduce excessive costs.

- Rewriting the Transmission Network Code from scratch

I should first include the mechanisms to facilitate the trade of capacity according to free market principles, both on a primary market and for a secondary market with transparent, flexible, fair and easy to implement mechanisms, including intra-day.

The Transmission Network Code should also:

- discipline the network users, relying exclusively on commercial principles:

- only the one who makes a mistake pays and only for its act in relation to responsibilities undertaken under contracts with the transmission operator,

- the price of mistake is the one set by the Romanian market at the time of mistake (not before or after the act, respectively exceeding the booked capacity by the network user and real imbalance of the national transmission system as a result of differences between quantities introduced and extracted from the system daily).

- have a legitimate speculative purpose, allowing the emergence of market players to sanction the indolence of users of the transmission network and act only in the margin, which prevents slippage by the National Transmission System to the impossibility to be used.

- limit the intervention of the transmission operator exclusively to the moment when market reaction (lack of reaction) determines reaching the early default limit of the system, using, again, exclusively the same commercial principles: only the one who makes a mistake pays and the price of the mistake is the one set by the Romanian market at the time of the mistake.

- establish the way in which the transmission operator will pay for its mistakes (failure to meet contractual conditions in terms of making available the booked capacity and ensuring the continuity in supply, if it is due to other network users), in relation to those who make mistakes, the price of the transmission operator’s mistake being also necessary to be determined by the Romanian market at the time of the mistake.

- The Distribution Network Code

Developing the Distribution Network Code, as a set of rules, by which the responsibilities and rights of the parties are set, as well as the manner in which gas flow continuity must be ensured, penalties charged or from which the user of the distribution system benefits, based on the same principles set out for the Transmission Network Code.

- The Storage Facilities Code

Developing the Storage Facilities Code, as a set of rules establishing the responsibilities and rights of the parties, as well as the way in which takeover/handover and storage/extraction of gas in/from storage are realized. Lack of detailed rules on the process of injection/extraction from storage facilities often leads to inequality in taking over own gas from the storage facilities: The Code of Storage Facilities has to start from the same principles as those set out for the Transmission Network Code.

- The Natural Gas Market Code

Developing the Gas Market Code (market model), containing clear rules, procedures and instructions in terms of gas trading and interaction of suppliers with shippers (allowing the monitoring of the flow in real time throughout the source-consumer circuit). Among the many elements that should be defined by this document, mechanisms for ensuring the flexibility and instruments for quick access of all participants thereto and the development of cheap systems to guarantee commercial operations are primary.

The Romanian gas market operates randomly, without a model that includes clear rules, procedures and instructions for gas trading. Currently, the lack of rules on correlation between trading actions and transmission, distribution, storage actions makes impossible to track gas flows from the acquisition point to the delivery point. Moreover, without these rules, matching procedures cannot be applied, essential procedures in the proper functioning of the market.

- Establishing the Balancing Operator.

The Romanian gas market operates almost exclusively depending on the outside temperature, contracts being put to the wall and making them useless. Therefore, only the transparency of contract conclusion, through transparent mechanisms (inclusively on the exchange), is useless without accountability for their compliance by the parties. Whenever the air temperature rises or falls, contract disappears in terms of rights and obligations. This is due to:

- Romanian mentality, lacking accountability;

- lack of flexibility mechanisms in the Romanian market, allowing the operation of contracts in accordance with their provisions;

- lack of balancing operator, having the responsibility, right and obligation to intervene in the market whenever necessary, applying the corrective methods, including penalties for those who create imbalances; as well as incentives.

The balancing operator, although provided for in the gas law to be achieved as role by the transmission operator, does not exist in the gas market. In absence of rules and a responsible entity (the law empowers the transmission operator, but it did not take this responsibility even after the installation of the private management), the market runs erratically, depending on temperatures and not on what is signed in contracts traded on the exchange. It determines, before imposing in the market certain trading obligations exclusively on the exchange, the need to impose and establish with priority this operator.

- Introducing mechanisms to ensure flexibility and functionality of the market.

As a contract signed, in order to operate it is necessary to develop secondary mechanisms to manage contract performance, which today are entirely missing. Mechanisms that should be legalized in the gas market are:

- Organization of the principal and secondary capacity market (of course, after determining the transmission and distribution capacity and after introducing the capacity reservation mechanisms in the distribution systems and in the injection/extraction points of storage facilities);

- The activity of gas storage in the transmission and distribution pipelines;

- Introducing the Gas Title and trading these titles, allowing a quicker and legal exchange of gas, even before its individualization by measurement and in absence of the supply license;

- Introducing certain mechanisms for borrowing or virtual storage of gas.

Without these mechanisms, contracts traded on the exchange cannot be efficiently executed, with potential losses for the signatory parties.

- Developing cheap guarantee schemes

The Romanian market, in general, and the gas market, especially – due to large amounts of money and low commercial margins, introduces an extremely high risk related to each transaction. Trading on the exchange will significantly increase this risk, through the behavior of certain participants that will appear in the market. At the same time, traditional guaranteeing instruments are extremely expensive and many of them are difficult to enforce, when an event occurs. Therefore, it is mandatory to introduce simple, cheap and easy to execute mechanisms. For example, warrant and certificates of deposit are simple and very useful elements in the natural gas market. (Warrant is a special certificate of gas storage with ordering character on the commodity, with which a transaction can be guaranteed. The certificate of deposit proves that the commodity is in the deposit).

- Computerization of gas market activity

Computerizing the activity in the gas market by developing systems for the storage and transmission of information between operators, suppliers, balancing market operator, gas exchanges, competent authority etc. Absence of computerized systems, at the level of market players, allowing the continuous monitoring, at least on a daily-basis, will make impossible the proper operation of the gas market and of the Codes.

Romania carries out activities in the gas market, before and after concluding the contract, through information manipulated by operators, which send data by telephone, with numerous omissions, delays, mistakes etc. Correlation between the data of sellers, buyers, operators is made in the same way, engineering being required to reach the closure of the monthly balance.

6. METHODS AND MEASURES FOR THE PROTECTION OF VULNERABLE CONSUMERS

Vulnerable customer, protected customer and household customer are notions that are confused in people’s minds. From a practical and legal point of view, there are major differences between these notions, which the new approach of the gas sector is mandatory to establish properly. If all vulnerable customers have to be protected, not all protected customers are vulnerable and even less so not all household customers are vulnerable.

Household customers (according to the gas law) are customers that buy natural gas for their own household consumption. To give more details, household customers are:

– customers using gas in order to heat their own spaces, to produce hot water and for cooking, in individual households and/or apartments, with individual metering;

– customers using gas in order to heat their own spaces, to produce hot water and for cooking, in individual households and/or apartments, with common metering;

– buildings for housing, no matter the ownership, under the administration of legal persons, public or private, including residential centers for people with disabilities, homes for the elderly, emergency children reception centers, maternal centers, boarding schools, dormitories which use gas for heating their own facilities, for cooking and hot water production.

Protected customers are customers for which gas supply must be ensured with priority, compared to other customers. Gas is an essential item of energy supply in the European Union, representing a fourth of primary energy supply and being mainly used for electricity generation, heating, as raw material for industry and fuel for transport. It determined the issue of Regulation no. 994/2010 of the European Parliament concerning measures to safeguard gas supply security (Regulation which is binding in all EU member states) and which defines protected customers as: all households connected to the gas distribution network and, furthermore, if the Member State so decides, they may also include: (a) small and medium enterprises, provided that they are connected to a gas distribution network, and essential social services, provided that they are connected to a distribution network or gas transmission network and that all of these additional consumers represent no more than 20% of total gas consumption; and/or (b) district heating plants to the extent that they supply energy to households and consumers mentioned in letter (a), provided that these plants cannot run on other fuels and are connected to a gas distribution or transmission network.

Vulnerable customers are customers which, for grounded reasons, cannot benefit from energy needed to ensure subsistence needs. Thus, these customers are found in the category of household customers, but those treated as household customers (hospitals, retirement homes, orphanages) can also be included in this category. The gas law in Romania gives the following definition of the vulnerable customer: end-customer belonging to a category of household customers which, for reasons of age, health or low income, risks social marginalization and which, in order to prevent this risk, benefits from social protection measures, including of financial nature.

If the capacity of household customer and that of protected customer do not change in time, a customer’s vulnerability is a state that can evolve from its existence to its non-existence.

Because among household customers the income level is different, the law in force requires highlighting as vulnerable customers only those household customers who truly need help. Absence of such an approach determines social inequity, because it makes “rich” household customers to benefit twice, once they are not vulnerable they should not benefit from these advantages and the second time because they benefit from a larger subsidy (having larger houses, more equipment or even pools that consume energy above the average consumption).

The system of regulated prices in Romania in fact brings all household customers in a situation of vulnerability, outside the legal framework, masking benefits for the “rich” customers to the detriment of the masses.

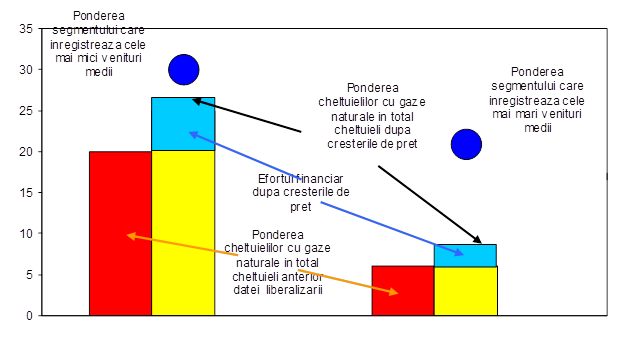

The share of gas expenses in the budget of poorer families, in winter months, is around 4 times higher than in the case of families with higher incomes.

Figure 12. The share of gas expenses in winter months in the budget of families with high income and those with very low income

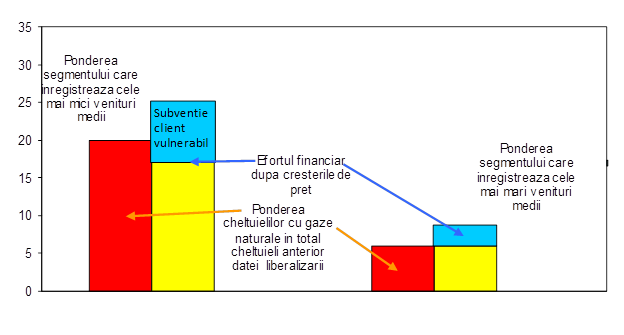

Eliminating regulated prices would bring additional revenues to the state budget, without a great burden on the budget of families with high income, but creating additional funds to the budget, enough to allow subsidizing a part of gas costs for vulnerable customers. Thus, we can get a decrease in the share of gas costs, in winter months, for customers with low income below the share of gas costs before market liberalization for household customers.

Figure 13. The share of gas expenses in winter months in the budget of families with high income and those with very low income, after applying the strategy of subsidizing vulnerable customers

Market liberalization for household customers, corroborated with the application of vulnerability criteria, would bring a lower cost (compared to the situation of regulated prices) with gas for really poor customers and would require an easily affordable increase for customers with high incomes.

Presenting this situation, in a persuasive manner, in the idea of the need to maintain regulated prices for household consumers is not for the benefit of large parts of the population of Romania, a poor population, but favors a small number of household customers, those with high incomes.

Legislation on gas consumer protection has developed, in order to protect the interests of gas consumers.

But the reality shows that they haven’t reached their goal. Gas customers don’t feel more protected today than a decade ago. Most of them feel the lack of protection in relation to gas suppliers, uselessness of any approach regarding gas supplied or services received, abuses they are subjected to by the “gas people”.

To a certain extent, this perception is grounded, operators activating in the market managing to place certain regulations by which they can avoid being held responsible by the technique of throwing the blame from one operator to another. But the absence of a real and applicable protection of gas consumers is due to them to a much greater extent. Lack of culture at individual level, but also at the level of companies, determines them to be afraid of suppliers, to refuse to act as a result of own beliefs and to remain unprotected.

Proposals for action

- Center of settlement of disputes in the gas market

Establishing an operational structure SALGAZ based on PPP (center for settlement of disputes in the gas market), according to Order 38/2015, with responsibilities in mediating any misunderstandings in the sources-consumption chain, but also in relation to other local, county and central bodies.

It is necessary to designate to the operational structure SALGAZ the role of information and dissemination in the gas market for end-consumers, in order to protect consumers and prevent abusive actions in the market.

2.1. Support measures for vulnerable customers

The philosophy of protecting vulnerable consumers should start from the following principles:

The consumer has to be accountable and helped pay the bills. Consumer protection starts by “helping” it to pay its gas bills and not by exempting it from payment.

Identifying consumers who cannot pay versus those who are not willing to pay. In Romania it was found that there are enough irresponsible people, who by presenting untruths receive undeserved benefits.

Measures taken to protect consumers should not lead to the vulnerability of the country. Practicing excessive exploitation of domestic gas resources, from the desire to have a lower price for end-consumers, leads to quick depletion of fields and may determine in the medium and long term to lack of energy security of the country.

The support mechanism for vulnerable customers includes in various European countries the following:

- Special payment arrangements for customers who cannot pay their bills (grace periods, equalizing annual bills etc.);

- Avoiding the disconnection from systems of consumers in certain periods of time;

- Financial support or social tariffs for certain categories of groups of consumers;

- Prepayment of gas and use of meters with coins or cards;

- Promoting energy efficiency measures among groups of customers, reducing energy consumption and determining their possibility to pay their utility bills;

- Block prices – including a low tariff for consumption up to a certain level, below market price and a much higher price than the market price fi that level of consumption is exceeded;

- Social subsidies for gas and electricity payment – amounts allocated for vulnerable consumers (it was proven that people often use this money for other needs, bills remaining unpaid), through schemes to subsidize suppliers from the local budget (with the downside that economic operators have the trend to introduce as many customers as possible in these categories, having the advantage of getting money for the commodity supplied without any risk) or payment by vouchers (method more efficient than the other ones, but at the same time bureaucratic and with very high costs).

Proposals for action.

- Programs of Governmental Strategy for the protection of vulnerable customers

We propose the initiation of social programs under government coordination for the partial payment of the gas amounts of vulnerable customers depending on criteria such as age, income, gas consumption, gas cost.

- Appointing an institution to apply and coordinate the protection of vulnerable customers

It is necessary to have an institution designated to coordinate the strategy of vulnerable customers protection, which involves social protection actions, fiscal measures, technical regulations, measures to cut energy consumption.

- Best practice code of suppliers licensed in the gas sector

It is necessary to implement a Best practice code of suppliers licensed in the gas sector, so that each supplier can develop its own mechanisms to help vulnerable consumers. Suppliers must present various methods for supporting these consumers, actions taken have to be mainly of preventive type, consultations and investments to consumers in order to reduce the inefficient energy consumption (insulation of homes, efficient insulation etc.) These measures have to be accompanied by tax exemptions for operations that make energy efficiency investments to vulnerable consumers in order to ensure their possibility to pay the bills.

- Prepayment of gas

It is necessary to implement prepayment of gas using smart meters, which determine a better connection between the financial capability of the consumer, the amount of gas consumed and environmental comfort.

- Flattening the gas payment curve.

It is necessary to flatten the gas payment curve during a calendar year, through specific formulas.

7. RETHINKING THE ACTIVITY OF DESIGN-EXECUTION-OPERATION OF OBJECTIVES IN THE GAS SECTOR AS ACTION INTENDED TO BOOST TRANSACTIONS

The activity of design in the gas sector should not be seen as burden for consumers or as a way to make profit by operators. This activity should be seen as it is, an activity related to that of gas sale, without profit or with a small profit; the purpose of design being exclusively to ensure the performance of the transaction, to ensure the minimum costs with the transport/distribution of gas from source to consumer, flexibility of market operation and security of supply.

Gas market liberalization should determine the development of a real market of services accompanying the activity of using gas:

- design;

- project verification and approval;

- construction of pipelines and installations;

- reception;

- exploitation of installations for using gas;

- verification of installations for using gas;

Proposals for action.

We believe it is necessary to entirely review the activity of design, construction and operation of infrastructure in the gas sector, as follows:

- Rethinking the system for the authorization of persons who are active in the field of design and construction

Romania is one of the few countries where the specialization of a person can be done not by school, but by exam, of multiple choice type. We believe that only graduates of schools for installations, transport and distribution of gas, school which allows them to acquire the knowledge necessary for design, execution and verification of installations in the gas sector.

We believe one should monitor the degree of training and development of technicians, which can be done similar to other professional activities in professional associations (such a structure is mandatory to be established in Romania).

- Conditioning multiple specializations at the level of the same person

Today, in Romania there are 16 categories of authorizations of a person activating in the gas sector, a person being able to be specialized in all fields (having the 16 categories of authorizations). The purpose of making this dissociation was to determine people to specialize in a single area. The normality should have determined each person to head to a single field, which did not happen, a single person replacing with authorization other 16, the difference being made only by paying 16 examination fees. Thus, we believe that under the law there should not be the possibility for a person to specialize in more than one field and only by leaving that field to be able to refocus on another field.

- Setting the incompatibility between the activity of design, verification and examination at the level of the same person

The activity of verification of projects and work verification (reception) are activities that should validate works performed by designers/executants, which determines the obligation of independence between the two categories. The situation now ubiquitous in which people from the same company that hold, one by one, the capacity of designer and verifier, mutually sign their projects, does not meet the conditions of objectivity. The same situation is necessary at the level of the activity of expertise – design/execution or expertise – verification.

- The obligation of examination by independent experts of works in the gas sector in conditions of opportunity, usefulness, feasibility, reliability, security, safety.

Works in the gas sector, which have a public nature (new construction/ modernization/ rehabilitation) have to be expertised by an independent expert, under the aspect of necessity/utility/profitability/efficiency/effectiveness/capacity/quality, so as to eliminate the current modality of wasting public money and/or unjustified increase in costs (tariffs) by operators authorized in the gas sector.

- Rethinking the philosophy of norms

Rethinking the regulations for design and operation, so as to allow a greater liberty (for the new designers), in choosing the solutions, as well as materials and procedures used, at least in the following cases:

- Eliminating projects for household installations for indoor use;

- Eliminating projects for household connections;

- Developing the design taking into account concepts of: reliability, maintainability, availability, preventive maintenance, stress tests etc.

- Permanent promotion of introducing the latest CE approved materials (copper pipes, relining etc.);

- Rethinking the pressure regimes in distribution systems, eliminating unnecessary pressure steps and increasing pressure in distribution systems to 16 bars, while setting the limit of 16 bars for gas transmission pipelines;

- Introducing new standards in terms of gas odorisation (including changing the odorant, which hasn’t fulfilled environmental requirements for over 10 years);