OMV Petrom Group: results for Q4 and January – December 2014

Q4/14 vsQ4/13

Mariana Gheorghe, CEO of OMV Petrom S.A.: “In 2014, we continued our stabilization effort, with the second year in a row of marginal hydrocarbon production increase yoy in Romania. In exploration, we have made the largest onshore and offshore investment since privatization. The success rate of our traditional exploration (excluding deep offshore) stood at 60%. We have resumed our drilling activity in the Neptun block with two new wells spudded, Domino-2 and Pelican South-1; in 2015, we will continue our exploration program as planned. In G&P, business challenges persisted due to lower gas market demand and negative spark spreads which led to a deteriorated result of the Brazi power plant. In R&M, we have successfully completed the Petrobrazi refinery modernization, which delivered the planned increase of USD 5/bbl in the indicator refining margin, contributing to a good end-year result, and strengthened the integration value of the company. In light of the volatile and potentially prolonged weaker market fundamentals, we are scaling back our investment plans for 2015 and have intensified cost optimization programs whilst maintaining our potential growth projects in the Black Sea. In 2015, we expect public consultations on the fiscal and regulatory environment to continue, as announced by the authorities, and we aim for a stable, predictable and investment-friendly framework, which is a key precondition for future investments.”

Business segments

Exploration and Production (E&P)

Fourth quarter 2014 (Q4/14) vs. fourth quarter 2013 (Q4/13)

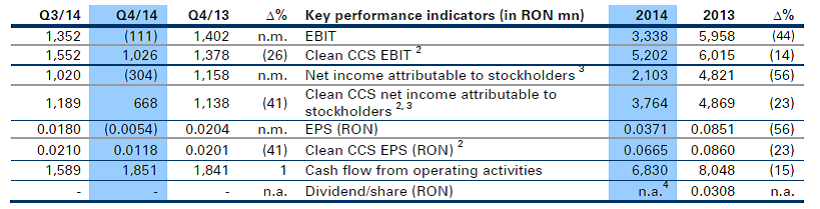

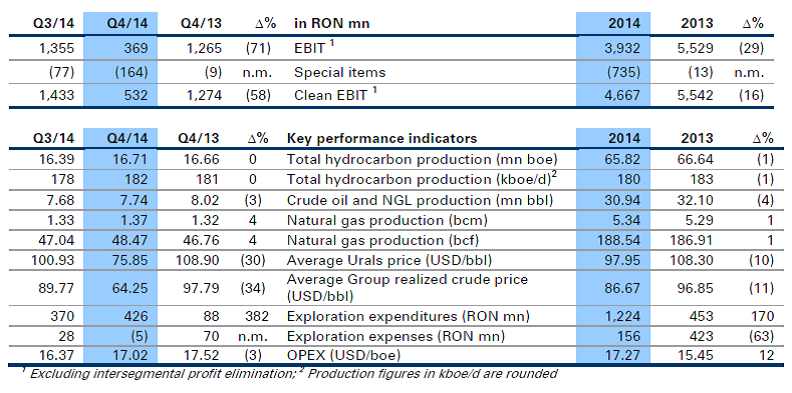

In Q4/14, the average Urals crude price decreased to USD 75.85/bbl, 30% lower compared to Q4/13. The average realized crude price also decreased by 34% to USD 64.25/bbl. Clean EBIT decreased by 58% to RON 532 mn in Q4/14, mainly due to lower oil sales in spite of favorable FX rates (USD 8% stronger against RON) and lower exploration expenses. When accounting for special items, mostly in relation to the impairment in Kazakhstan triggered by unsuccessful field redevelopment results in the TOC fields and the restructuring provision in Romania, reported EBIT stood at RON 369 mn, 71% below the level of Q4/13. Group production costs (OPEX) in USD/boe decreased by 3%, mainly resulting from by favourable FX rates and slightly higher production in Romania. In Romania, production costs decreased by 4% in USD/boe, while, in RON terms, they were 4% above the Q4/13 level, predominantly due to new construction tax introduced in 2014. Exploration expenditures increased to RON 426 mn, mainly in relation to the drilling of Domino-2 and Pelican South-1 in the deep offshore Black Sea. Exploration expenses amounted to RON (5) mn, in Q4/14, mostly due to a reclassification of project costs. Group daily hydrocarbon production was 181.6 kboe/d (of which 172.2 kboe/d in Romania) and total production stood at 16.7 mn boe, reflecting slightly higher production in Romania and lower production in Kazakhstan. In Romania, total oil and gas production stood at 15.85 mn boe, 1% above the Q4/13 level (15.68 mn boe). Domestic crude oil production was 6.96 mn bbl, 3% below the Q4/13 level (7.20 mn bbl) due to planned workovers and weather conditions. Domestic gas production was higher at 8.89 mn boe, mostly supported by the new wells put on stream in the Totea and Mamu fields. In Kazakhstan, production amounted to 0.86 mn boe, 12% lower compared to the same period of 2013, mainly reflecting steep natural decline of key fields. Hydrocarbon sales volumes have slightly increased compared to Q4/13, mainly triggered by the higher gas sales volumes in Romania and oil sales in Kazakhstan. In Q4/14, we finalized the drilling of 41 new wells and sidetracks, compared to 38 new wells performed in the same quarter last year.

Fourth quarter 2014 (Q4/14) vs. third quarter 2014 (Q3/14)

Clean EBIT decreased by 63% in Q4/14 mostly due to lower oil prices, which offset the favorable effect from FX rates (USD 7% stronger against RON). Reported EBIT dropped 73% below Q3/14, also reflecting higher special items. Group production costs in USD/boe increased by 4% compared to Q3/14 level. Production costs in Romania increased by 4% when expressed in USD/boe, and by 10% in RON/boe terms (RON 58.05/boe), as Q4/14 was mainly influenced by costs related to increased services and maintenance activity. Exploration expenditures increased by 15% to RON 426 mn mainly due to intensified drilling activity in the Black Sea. Group daily production stood at 181.6 kboe/d while total production was 16.71 mn boe (Q3/14: 16.39 mn boe), with increased production in Romania and in Kazakhstan. Group sales volumes increased by 2% compared to the Q3/14 level, largely due to higher sales in Kazakhstan and higher gas sales in Romania.

January – December 2014 vs. January – December 2013

Average Urals crude prices decreased by 10% compared to 2013 to USD 97.95/bbl. The average Group realized crude price was USD 86.67/bbl, 11% lower than in 2013. Clean EBIT went down by 16% to RON 4,667 mn, mainly driven by lower oil and NGL sales and higher production costs. Reported EBIT reached RON 3,932 mn, 29% lower than 2013, due to higher special charges which were mostly related to impairments in Kazakhstan triggered by unsuccessful field redevelopment results in the TOC fields. Group production costs in USD/boe of USD 17.27/boe, were 12% higher, compared to the 2013 level, reflecting the higher production costs in Romania and lower production for sale in Kazakhstan, in spite of favorable FX rates. Production costs in Romania expressed in USD/boe were USD 16.84/boe, 13% higher than the 2013 level, while in RON terms they increased by 13% to RON 56.32/boe, mostly due to the new construction tax introduced in 2014 and higher personnel costs. Exploration expenditures reached RON 1,224 mn, which mainly include the capitalized expenditures in relation with the drilling activities in the Black Sea associated with Domino-2 and Pelican South-1. Exploration expenses amounted to RON 156 mn in 2014 and were down by 63% mostly due to less seismic works in 2014 and lower drilling write-off, while 2013 was influenced by the largest ever 3D seismic campaign in the Romanian sector of the Black Sea. Group oil, gas and NGL production in 2014 totaled 65.82 mn boe, 1% lower than the 2013 level as a result of decreased production in Kazakhstan. In Romania, total oil, gas and NGL production increased to 62.57 mn boe, slightly higher compared to the previous year. Domestic crude oil production was 27.98 mn bbl, 2% lower than 2013 due to planned workovers and weather conditions. Domestic gas production reached 34.58 mn boe, 2% higher compared to 2013. Oil and gas production in Kazakhstan decreased by 21% to 3.25 mn boe, as an effect of technical constraints. Group sales volumes were slightly lower compared to the 2013, supported by the higher gas sales in Romania. As of December 31, 2014 the total proved oil and gas reserves in OMV Petrom Group’s portfolio amounted to 690 mn boe (of which Romania had 671 mn boe), while the proved and probable oil and gas reserves amounted to 977 mn boe (of which Romania had 930 mn boe). The Group’s three-year average reserve replacement rate decreased to 39% in 2014 (2013: 48%), in Romania it also decreased to 39% (2013: 48%). For the single year 2014, the Group’s rate was 42% (2013: 31%), while the reserve replacement rate in Romania was 42% (2013: 32%), mainly as a result of exploration and appraisal wells, reservoir studies performed and better performance of new drilled wells.

Gas and Power (G&P)

Fourth quarter 2014 (Q4/14) vs. fourth quarter 2013 (Q4/13)

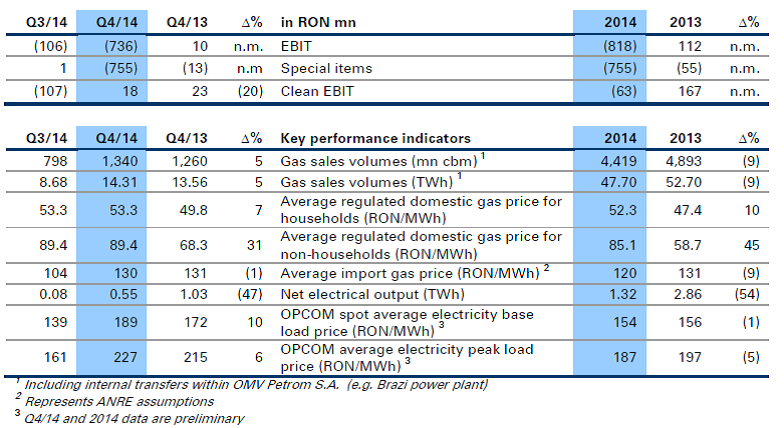

Clean EBIT decreased by 20% to RON 18 mn, reflecting the deteriorated negative contribution of the power business, partly mitigated by the improved result of the gas business. The latter was supported by the reversal of a RON 30 mn provision for outstanding receivables in Q4/14. Reported EBIT significantly decreased to RON (736) mn, mainly reflecting the impairment of the Brazi power plant due to the revised long-term market perspective. National estimated gas consumption remained almost unchanged, while OMV Petrom’s gas sales volumes increased by 5% compared to Q4/13, triggered by higher sales to the fertilizer industry, which more than compensated the reduced Brazi power plant utilization. At the end of Q4/14, the total volume of natural gas stored by OMV Petrom amounted to 405 mn cbm compared to 160 mn cbm at the end of Q4/13 due to lower market demand in the injection period. In Q4/14, the regulated domestic gas prices remained unchanged versus Q3/14 (RON 89.4/MWh for the non-household sector and RON 53.3/MWh for household consumers), but increased versus the Q4/13 levels. On the Romanian Commodities Exchange, the price of natural gas from domestic production varied between RON 84.9/MWh and RON 88/MWh for contracts signed and gas delivered in Q4/14. The average import gas price based on ANRE estimate was USD 400/1,000 cbm (or the equivalent of RON 129.6/MWh). The average import quota set by ANRE for the non-household sector was 5% in Q4/14, significantly lower compared to an average of 18% in Q4/13. National estimated gross electricity production increased by almost 5% versus the same quarter of last year, while the estimated national electricity demand remained relatively stable, Romania thus maintaining its position as net exporter of electricity (estimated export – import net balance of 2.2 TWh) in Q4/14. According to preliminary data published by OPCOM, the base load electricity price averaged RON 189/MWh, while the peak load electricity price averaged RON 227/MWh. The net electrical output generated by the Brazi power plant was 0.52 TWh in Q4/14 (Q4/13: 1.00 TWh), due to weakened spark spreads following the significant increase in the gas price. In Q4/14, the Dorobantu wind park had a net availability of 99% and delivered a net electrical output of almost 0.03 TWh, 14% higher than in Q4/13. For the electricity produced and delivered to suppliers, OMV Petrom Wind Power S.R.L. received ~41,300 green certificates, half of which are expected to become eligible for sale after January 1, 2018 (Q4/13: ~39,100 green certificates, half of them eligible for sale).

Fourth quarter 2014 (Q4/14) vs. third quarter 2014 (Q3/14)

Compared to Q3/14, Clean EBIT significantly improved in Q4/14, due to the positive contribution of the gas business, which was supported by the reversal of the RON 30 mn provision for outstanding receivables booked in Q3/14. Estimated national gas consumption seasonally increased by 136% versus Q3/14, while OMV Petrom’s gas sales volumes increased by only 67%, due to a portfolio mainly consisting of industrial consumers, which are less sensitive to seasonality. The net electrical output of the Brazi power plant increased by 0.45 TWh compared to Q3/14 driven by favorable spark spread development, which allowed the Brazi power plant to be utilized for gas value chain optimization, in line with our strategic direction. Net electrical output of the wind park Dorobantu seasonally increased significantly.

January – December 2014 vs. January – December 2013

Clean EBIT declined significantly to RON (63) mn in 2014 compared to RON 167 mn in 2013, largely due to the negative power business contribution as a result of average negative spark spreads triggered by higher gas prices and slightly lower average electricity price. In addition, the contribution of the gas business was lower versus 2013 mainly due to lower gas sales volumes and increased storage costs (new transportation tariff and higher volumes). Reported EBIT of RON (818) mn reflected special items of RON (755) mn mainly related to the Q4/14 impairment of the Brazi power plant. Total estimated gas consumption in Romania decreased by around 4% versus 2013 mainly due to lower demand from the chemical industry and mild winter. OMV Petrom’s consolidated gas sales declined by 9%, which reflects the reduced off-take by heat and power plants compared to 2013. Estimated national gross electricity production increased by almost 9% in 2014 versus 2013, while the estimated consumption remained relatively stable. The preliminary export – import net balance reached the record level of 7.2 TWh, also supported by regional market coupling starting November 2014. According to preliminary data published by OPCOM, electricity prices on the Romanian day-ahead market averaged RON 154/MWh for base load and RON 187/MWh for peak load in 2014. In 2014, the total net electrical output of the Brazi power plant was 1.22 TWh (2013: 2.74 TWh), covering ~2% of Romania’s electricity production over the full year and ~6% of the balancing market (2013: ~5% of Romania’s electricity production and ~9% of the balancing market) according to estimated available information. The Dorobantu wind park generated a net electrical output of 0.08 TWh versus 0.10 TWh in 2013. For the electricity produced and delivered to suppliers, OMV Petrom Wind Power S.R.L. received ~133,000 green certificates, half of which are expected to become eligible for sale after January 1, 2018 (2013: ~178,000 green certificates, thereof ~32,000 eligible for sale after January 1, 2018).

Refining and Marketing (R&M)

Fourth quarter 2014 (Q4/14) vs. fourth quarter 2013 (Q4/13)

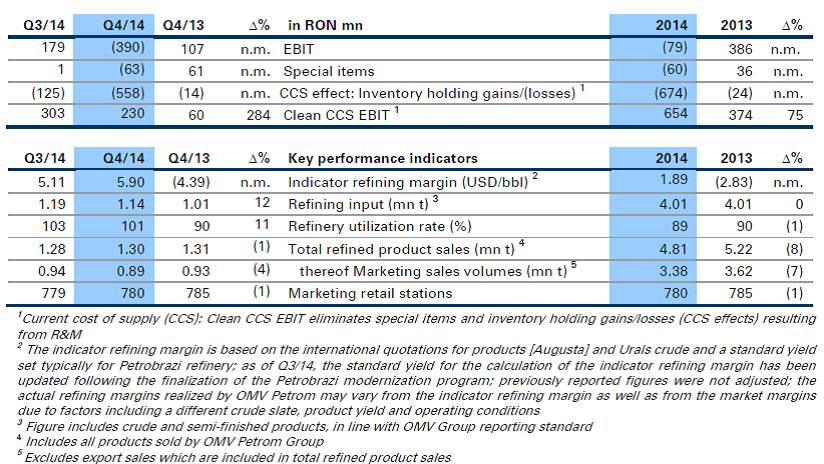

In Q4/14, clean CCS EBIT increased to RON 230 mn, supported by strong refining margins, better operational performance after the refinery modernization and an improved marketing result. Net special items at the amount of RON (63) mn were recognized in Q4/14 related to the impairment of marketing assets in the Republic of Serbia. Decreased crude oil prices and lower product quotations led to a negative CCS effect of RON (558) mn, resulting in a reported EBIT of RON (390) mn. The updated standard yield combined with lower cost for crude, resulted in the indicator refining margin at USD 5.90/bbl level in Q4/14 versus USD (4.39)/bbl in Q4/13. The refinery utilization rate increased to 101% (90% in Q4/13), reflecting a temporarily higher throughput run given a high level of crude stock after mid-year planned shutdown. Consequently, the total quantity of refining input increased in Q4/14 by 12% compared to the level recorded in Q4/13. Total refined product sales slightly decreased reflecting lower market demand. In addition, OMV Petrom had to build and maintain increased levels of compulsory stocks of oil products, above our previous optimum inventory levels. Total group marketing sales volumes in Q4/14 were 4% below the Q4/13 level. Group retail sales, which accounted for 69% of total group marketing sales, decreased by 2% compared to Q4/13, mainly impacted by increased fuels taxation in Romania and higher competition. Commercial sales dropped by 7% reflecting lower sales of diesel due to competition, with challenging bitumen and fuel oil market in the region. At the end of Q4/14, the total number of filling stations operated within OMV Petrom Group decreased by 5 units to 780 compared to Q4/13, mainly as a result of retail network optimization in Bulgaria initiated in mid- 2014.

Fourth quarter 2014 (Q4/14) vs. third quarter 2014 (Q3/14)

Clean CCS EBIT decreased in Q4/14 compared to Q3/14, driven by a seasonally lower marketing sales and oil product mix. The refinery utilization rate stood at 101% while the indicator refining margin increased to USD 5.90/bbl in Q4/14 from USD 5.11/bbl in Q3/14, mainly as a result of lower cost for crude.

January – December 2014 vs. January – December 2013

Clean CCS EBIT significantly improved to RON 654 mn compared to RON 374 mn in 2013, supported by increased refining margins, improved operational performance after the refinery modernization and good marketing result. In 2014, we registered the first year with positive results in both business segments, reflecting the company’s commitment to improve operational performance, to further pursue cost discipline and optimization of the downstream business. The indicator refining margin increased to USD 1.89/bbl, from USD (2.83)/bbl in 2013, reflecting the updated standard yield following the completion of the Petrobrazi refinery modernization program and lower cost for crude . In 2014, the refinery utilization rate stood at 89% reflecting the one month planned refinery shutdown in Q2/14. Total marketing sales volumes decreased by 7% compared to 2013, affected by the increased taxation in Romania and higher competition in our operating region. In retail, Group sales volumes dropped by 4%, while commercial sales volumes fell by 11%, the negative trend being reflected in all products except gasoline and jet.

Outlook 2015

Market, regulatory and fiscal environment

We expect the Brent oil price to average between USD 50-60/bbl. The Brent-Urals spread is anticipated to stay relatively tight. The gas and power markets and regulatory framework are undergoing continuous changes that may adversely impact the company’s financial and operating results. In 2015, gas demand in Romania is not expected to recover, which will lead to increased competition and further margin pressure. Regulated gas prices and import obligation for non-household consumers have been abolished starting January 2015, while the price for domestic production to be paid by regulated households during H1/15 was set at RON 53.3/MWh (EUR 12.0/MWh), unchanged since July 1, 2014. The same price applies for the domestic gas volumes which Romanian gas producers are obliged to supply to the district heating sector (only for the quantities used to produce heat for household consumption). In addition, gas producers and suppliers must sell via Romanian centralized trading platforms up to approximately one third of their domestic gas quantities for the free market, which has proven to be a challenge in 2014. In the power market, demand is anticipated to be relatively stable and prices to remain under pressure. In 2015, refining margins are expected to come down from the recent highs, due to persisting overcapacity in local and European markets. Due to the decreased oil price, lower product prices are expected to support the demand in the marketing business, nevertheless with increased competition. The package of fiscal measures introduced starting February 2013 imposing a supplementary taxation for oil and gas producers was extended for 2015. In addition, the constructions tax was reduced to 1.0% from 1.5% in 2014. This year, we expect public consultations with respect to upstream oil and gas taxation envisaged to be applicable starting 2016, as publicly announced by the authorities. Our aim remains to achieve a long term, stable and investment-friendly taxation and regulatory framework, a key precondition for future investments.

OMV Petrom Group in 2015

- CAPEX for 2015 is currently expected to be in the range of EUR 0.8 – 1.1 bn, of which approx. 85% will be dedicated to E&P;

- Intensified cost optimization programs across all business segments to be prepared for a potentially prolonged low oil price environment;

- Management intends to propose allocation of dividends for the 2014 financial year, subject to further approval by the Supervisory Board and the Annual General Meeting of Shareholders.

Exploration and Production

- We will continue our operational excellence initiatives focusing on efficiency, also taking into account the market operating environment;

- Operational activities will focus on delivering around 1,200 workovers and up to 70 new wells, dependent on market and fiscal environment;

- Value based prioritization of the FRD projects; projects under development/execution will be slowed-down, while those under appraisal phase will be re-engineered or reduced;

- Joint venture with Repsol: exploration drilling for two exploration wells is on-going; other two leads expected to progress;

- Joint venture with Hunt Oil: Padina Nord discovery to further advance; development options are under consideration;

- Joint-venture with ExxonMobil for Neptun Deep: Pelican South-1 well exploration operations on- going, expected to be completed in Q1/15; Domino-2 drilling completed; further exploration and appraisal drilling is expected in 2015. Domino-2 and Pelican South-1 results together with data from additional exploration wells will be used for the evaluation of the consolidated block potential;

- In Kazakhstan – further pursue water injection schemes in both the TOC and Komsomolskoe fields in order to secure reservoir pressure support and slow down the natural decline of production, planned to be finalized in H1/2015.

Gas and Power

- The gas value chain will be optimized in an integrated manner so as to dynamically address challenges in the market and maximize value creation;

- Continued pressure on spark spreads is anticipated, which may lead to a negative result of the power business in 2015; in this context, the focus will be on strict cost management, portfolio optimization and capturing available market opportunities by capitalizing on the Brazi power plant operational flexibility;

Refining and Marketing

- We will further capitalize on the successful completion of the Petrobrazi refinery modernization along the whole value chain; moreover, the refinery will continue economic energy efficiency improvements;

- The fuel terminal network optimization program will continue with the reconstruction works at the Cluj terminal expected to be finalized by the end of 2015;

(bvb.ro, February 19th)

Recent Comments