Home / Natural Gas /

Does the decrease in import gas prices reduce Romania’s energy independence?

by Dumitru Chisalita, energy expert

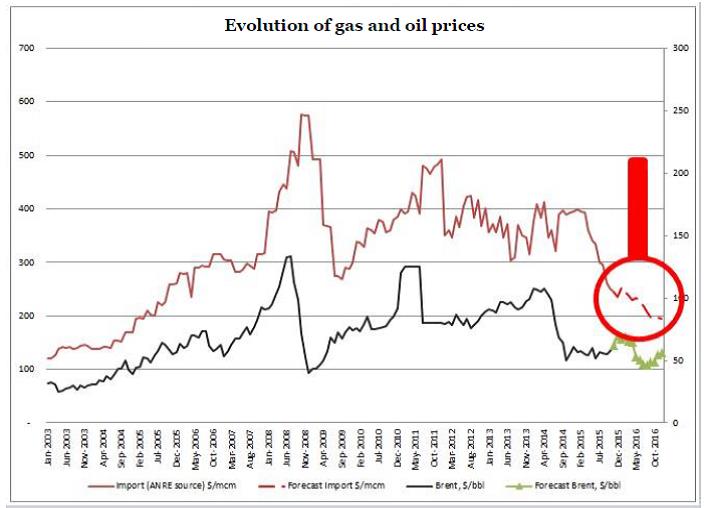

In the recent years, some analysts have appreciated the important steps in Romania’s energy independence, even if the truth shows that this independence was conjectural, caused by the closure of industrial consumers and not public policies. Can an important decrease in import gas prices throw Romania at any moment in the position of reliance on gas imports? Both positions are conjectural and it is important for Romania to eliminate the obsolete concept of energy independence and replace it with the concept of energy security. In this regard, I make reference to dangers posed by this concept described in an article written in 2013, called Energy security vs. energy independence (http://dumitruchisalita.ro/2013/12/28/securitate-energetica-versus-independenta-energetica/). Contrary to some beliefs in the market, in my opinion cutting the price of Russian gas supplied to Europe is not a decision with an argument, decisively extra-commercial. In my opinion, the trend of gas prices, corroborated with the price of petroleum products, which are linked by formulas existing in gas sale-purchase contracts, show since 2014 a trend to reduce gas prices, which could reach in 2016 values of USD 200/TCM. In fact, it is an estimate of mine presented in early 2015 in the book “Piata gazelor naturale” (The Gas Market), Transilvania Brasov Publishing House, showing the possibility that in 2016 gas prices could reach USD 200/TCM.

I believe that a price of gas of USD 200/TCM is not likely to endanger Gazprom. I believe that even if this company will face an important decrease in revenues, this price level is far from being a survival problem for Gazprom. At the same time, I believe that the decrease in import gas prices to this level is an important lesson that countries such as Romania should learn.

Some of these lessons are:

- The free gas market is an extremely volatile market – the decrease in import gas prices in 3 years by approximately 300%, which the participants should be able to manage, especially within a few dozen months in which the price will start to grow,

- Admitting the danger represented by the concept of energy independence, which can determine situations in which the cost of energy produced in Romania is higher than the imported one. Thus, security is endangered by the lack of competitiveness of products made in Romania. Last but not least, transport channels (transmission, distribution networks etc.), in conditions of discovering new resources in the Black Sea, require important changes and investments which can make gas prices to end-consumers to exceed the price of imported gas. Thus, eliminating imports may create energy independence, but not energy security.

A company of Gazprom size has an important margin, in conditions of reduced gas demand, having the interest of keeping its market share and imposing new directions. The current “energy games’ will have effect in the next 5-10 years and will be decisive for the next 20-30 years as access to sources, access to transmission routes and positioning in the energy markets. As shown in numerous materials, the so-called energy independence of Romania is a conjectural phenomenon, unsustainable in the long run. The most important proof of the ephemeral energy independence of Romania is that when the price of Russian gas decreases below the price of gas produced in Romania we will suddenly notice that Romania will import gas. In fact, the rules of the free market will always determine the choice of the gas source with the lowest price, regardless of its origin. Romania has an import capacity which can cover entirely the current gas consumption. An evolution in prices for imported gas to the level of USD 200/TCM will increase competition in terms of sources, with the possibility to set the final price on the Romanian market around this value or maybe even lower. The wholesale market, in terms of sources, will face a strong competitive phenomenon, which will also bring lower prices for gas purchases. As a result, the revenues of producing companies will fall, with two immediate main consequences: cutting investments and reducing incomes from taxes, royalties, dividends, corporate taxes etc. to the state budget. In this context, the project of new taxes in the gas sector comes late and entirely inconsistent with market realities. In the past 5 years, when margins in this sector were important, there was no important change in these taxes, and now a document is proposed that is not adapted to realities. Another worrying element for Romania, which is in full process of developing important projects in both upstream and in the development of transmission pipelines, is that the important change in gas prices in a market has impact on all present and future projects. I wrote in an article published in 2013: It is necessary to redesign the transmission system, so that gas transit from West to East and from South to North and the vice versa could ensure the necessary energy as support for transmission and balancing between various areas, in conjunction with the development of local systems, allowing the takeover of gas from local fields and its transmission on relatively small distances. This approach must be possible from a technical point of view and attractive in terms of tariffs charged. Redesigning the transmission system from several points of view: – legally (separate rules for each system category), – technically (technological regimes, investment, operational and maintainability approaches different on system categories), – economically (tariff methodologies, royalties, taxes, separate tariffs for system categories) would allow taking over gas from local fields and transporting it depending on pressures available, but also bidirectional transit through a national system compatible with the transmission systems of neighboring states, taking over gas discovered in new conventional and unconventional gas fields, interconnection with the current and future gas transmission systems, it would ensure the functioning of the gas sector in line with the business principles promoted by the European Directives and Regulations, the economic development of Romania and its energy security, including by reducing energy dependence. This is the approach that can shelter us from multiple repositioning that will permanently appear in the future gas market, determined by price volatility, by the volatility of supply and demand. Apparently, consumers should enjoy that a cheaper gas from import will determine a competition of gas sources and cause an alignment of gas prices according to the lowest price offered. I believe that a decrease in the price of imported gas to a level of USD 200/TCM will lead to a decrease in prices on the wholesale market, the supply market of suppliers, traders and large consumers. In turn, it is my opinion that there will not be a significant influence on gas prices to end-consumers. Lack of competition in the retail market will prevent the apparition of lower prices at the level of end-consumers. This situation will favor gas suppliers, which will increase their profits. Losers of this scenario will be the consumers, the state budget and the producers. In 2015, from my calculations it resulted the decrease in gas prices in the last 9 months by around 10% at the level of their acquisition by suppliers and trades, but this decrease was not found in the decrease in gas prices at the level of end-consumers, where I estimate that in the same period the price of gas increased on average by around 0.5%. Islanding the gas market in Romania, decreasing gas demand, oversupply of gas, competition on the wholesale market and other factors were reflected in the decrease in the purchase price for suppliers and traders. Lack of competition in the retail market will prevent the apparition of lower prices at the level of end-consumers. Two years ago I stated in another article: Gas market liberalization involves the elimination of the monopolistic position of companies acting in this field, eliminating the possibility to influence the gas price in the market, directly or indirectly, but first requires consumer information. As long as consumers fail to gain minimum specific knowledge allowing a proper evaluation of gas purchased, they will remain “captive” even in the liberalized market. In fact, there is a great risk for the liberalized market to turn into a market of smart suppliers, which would benefit indirectly from liberalization, i.e. taking advantage of the lack of information at consumer level, fully benefiting from the financial effects that such a market would produce. The liberalized gas market without informed consumers, encouraged to intervene, supported to negotiate, able to analyze various offers, determined to act responsibly, cautiously and without allowing constraints, will only be another disappointment for the Romanian people. Unfortunately, what I estimated at the time we see as results today. The shortsightedness of state institutions responsible for the obvious realities in the gas market is dangerous. I believe that the evolution of import gas prices is based on commercial reasons, in line with the strategy of the Russian concern on the European market, which can significantly influence the market and the gas activity in Romania. But, at the same time, it is my opinion that a possible non-commercial decision can be made at any moment, which would have an incomparably greater impact on Romania, highlighting once again how vulnerable and unable we are in ensuring energy security, including diminishing energy poverty.

Source: www.dumitruchisalita.ro

Image courtesy of Stuart Miles at FreeDigitalPhotos.net

Recent Comments